ℹ️ Note: This article is for general educational and informational purposes only. All budget figures, spending examples, and psychological research references are illustrative. Individual spending patterns vary significantly. RozHisab is a personal finance tracking tool — not a financial advisory service.

Let's reconstruct a completely normal Tuesday evening in urban India.

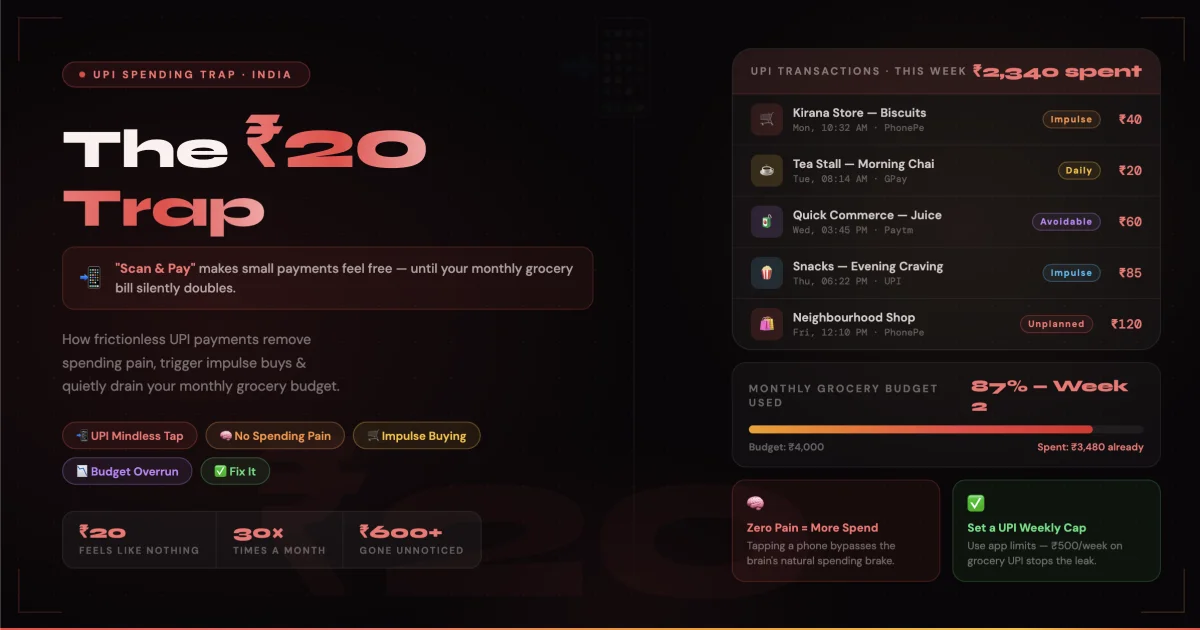

You stop at the vegetable vendor outside your building. Tomatoes, onions, coriander. ₹85. Scan. Pay.

Walking back, you pass the juice stall. It's hot. Sugarcane juice. ₹40. Scan. Pay.

Neighbour mentions the new biscuit arrived at the kirana. You pick up two packets while you're there. ₹60. Scan. Pay.

That evening, recipe needs coconut milk. Quick trip out. ₹35. Scan. Pay.

Nothing unusual. Nothing unreasonable. Total for the evening: ₹220.

Now multiply that Tuesday by every day of the month. Add the morning chai stop, the afternoon snack, the weekend "just picking up a few things," the impulse nimbu pani on the commute.

By the 30th, you've spent ₹4,800 more than you budgeted on groceries and food — and you have absolutely no memory of where it went, because every individual transaction felt completely reasonable.

This is the ₹20 trap. And UPI Scan and Pay is its primary delivery mechanism.

What Is Digital Payment — And Why It Changed Spending Psychology Forever

What Is Digital Payment

What is digital payment: A digital payment is any financial transaction completed electronically — without the use of physical cash. In India, digital payments are now deeply integrated into daily life at every level of the economy — from a ₹5 vada pav stall in Mumbai to a luxury hotel in Delhi.

Types of Digital Payment in India

Types of digital payments used by Indian consumers:

- UPI (Unified Payments Interface): Scan and Pay, UPI ID transfer, phone number payment via PhonePe, Google Pay, Paytm, BHIM. The dominant payment method in India — over 13 billion transactions per month as of 2026.

- Debit card: Tap or swipe at POS terminals. Linked directly to savings account.

- Credit card: Tap or swipe. Payment deferred to billing cycle. Rewards on spending.

- Mobile wallets: Paytm Wallet, Amazon Pay — pre-loaded digital balance.

- Net banking: Browser-based transfer. Used for larger transactions.

- NEFT/IMPS/RTGS: Bank-to-bank transfers. Not typically used for daily grocery purchases.

For daily grocery and food spending — the category we're examining — UPI Scan and Pay dominates. And it is specifically this payment type that most directly enables the ₹20 trap.

The Advantages of Digital Payment — And the Hidden Cost Nobody Mentions

Advantages of digital payments are real and significant: no need to carry exact change, instant payment confirmation, transaction history automatically recorded, no risk of losing physical cash, available 24/7 at virtually every merchant in India.

Benefits of digital payment are also well documented: financial inclusion, reduced black money, lower transaction costs for merchants, faster settlement, and the convenience that has made India one of the world's largest digital payment markets.

These advantages are genuine. But they come with a psychological side effect that nobody in the "India going digital" narrative talks about openly:

Digital payments — especially UPI Scan and Pay — are specifically designed to reduce the psychological friction of spending money.

That friction reduction is what makes digital payments convenient. It is also what makes them dangerous for budget discipline.

The Psychology of Impulse Buying Behaviour — Why Your Brain Loves UPI

Impulse Buying Behaviour — What Research Shows

Impulse buying behaviour is defined as unplanned purchasing — buying something you didn't intend to buy before you encountered it or the opportunity to buy it.

Consumer behaviour research has consistently shown that impulse buying increases significantly when payment friction decreases. This is not a new finding — it's why credit cards and supermarket checkout lines were specifically designed the way they are.

But UPI Scan and Pay takes friction reduction to a new extreme:

- No wallet to open: Physical cash requires opening a wallet, selecting notes, counting change — three micro-decisions that each provide a moment of spending awareness

- No PIN for small amounts: Transactions under ₹500 often require no PIN or biometric — just scan and confirm with one tap

- No physical sensation of loss: Handing over a ₹100 note creates a tangible, physical sense of "this money is leaving me." Scanning a QR code creates no comparable sensation — the money is abstract until you check your balance

- No visual depletion: A physical wallet getting thinner through the day is a visible signal that you're spending. Your UPI app balance doesn't deplete visually — you have to actively check it

The result: the average decision time for a UPI Scan and Pay transaction is under 8 seconds. The average decision time for a cash transaction of the same amount is 22–30 seconds — including the time to assess whether you have the right denomination and whether you want to break a larger note.

Those 14–22 extra seconds of cash friction are where budget discipline lives. UPI has eliminated them.

The ₹20 Trap — Why Small Amounts Are the Most Dangerous

The trap is not the ₹500 grocery order you plan for. It's the ₹20, ₹35, ₹50, ₹80 transactions that happen without planning, without awareness, and without any individual one feeling significant.

The mathematics of micro-transactions:

- ₹20 daily chai from the stall

near your office:

Daily: ₹20 | Monthly: ₹520 - ₹35 nimbu pani / coconut water

on commute (4x per week):

Weekly: ₹140 | Monthly: ₹560 - ₹60 impulse biscuits/snacks

at kirana (3x per week):

Weekly: ₹180 | Monthly: ₹720 - ₹80 "just a few things" trips

that weren't on the shopping list

(8x per month):

Monthly: ₹640 - ₹45 extra vegetables bought

because they "looked fresh"

at the street vendor (6x per month):

Monthly: ₹270

Total monthly micro-transaction grocery and food overspend: ₹2,710 per month.

This is ₹32,520 per year in unplanned grocery and food spending — on transactions none of which individually felt significant.

None of these purchases required going to a store, making a decision, or even slowing down significantly. All of them happened in under 8 seconds each with UPI Scan and Pay.

Why Your Grocery Expenses Keep Growing Even When You're "Being Careful"

Most households that struggle with grocery expenses are not irresponsible spenders. They are careful people whose careful intentions are undermined by a payment system specifically engineered to bypass careful intentions.

Three patterns that cause grocery expenses to balloon with digital payments:

Pattern 1 — The Invisible Accumulation:

You never make one bad decision.

You make forty-seven small,

individually reasonable decisions.

The problem only becomes visible

when the month-end total appears.

By then the money is spent

and the patterns are already

set for next month.

Pattern 2 — The Mental Accounting Failure:

Most people mentally track their

"big" grocery shop (the weekend

supermarket trip or the weekly

vegetable market run) but not

their daily micro-transactions.

The big shop is budgeted for.

The micro-transactions are not.

The micro-transactions often

equal or exceed the big shop over a month.

Pattern 3 — The Availability Effect:

When cash was the primary payment method,

not carrying cash was an automatic

spending brake. You'd pass the

chaat vendor and think "I don't

have change" — and keep walking.

With UPI on your phone, you always

have money available for any

transaction at any merchant

who accepts QR code payment —

which in urban India is now

virtually every street food vendor,

kirana store, and vegetable seller.

The House Monthly Budget Problem — Grocery Edition

The house monthly budget for a typical urban Indian family of 4 typically allocates ₹8,000–₹14,000 for groceries and household staples. When we ask most households how much they actually spent, the number is typically ₹11,000–₹18,000.

The gap — ₹3,000–₹4,000 per month in most households we speak to — is almost entirely composed of untracked micro-transactions made via UPI Scan and Pay.

How to prepare a family budget for a month — the grocery section that most templates get wrong:

Most family budget templates (including the "prepare a family budget for a month project PDF" templates available online) have one line for groceries with one monthly number. This is structurally insufficient for how Indian households actually buy groceries.

A realistic Indian household grocery budget has at least 4 lines:

- Planned grocery shop (weekly market / supermarket): This is the budgeted, intentional spend

- Fresh produce micro-purchases (street vendor, daily vegetables): Small, frequent, easy to underestimate

- Food and snacks outside home (chai, snacks, nimbu pani): Often mentally categorised as "not groceries" but directly competes with the same budget

- Kirana impulse purchases: The items that weren't on the list but "we needed them anyway"

Only when you track all four lines separately do you see where the budget is actually leaking.

Top 10 Brilliant Money Saving Tips to Counter the ₹20 Trap

These are not generic money saving tips. They are specifically designed to counter the impulse buying behaviour enabled by UPI Scan and Pay — while keeping the genuine advantages of digital payments.

1. Set a daily UPI spending limit

notification:

Most banking apps allow you to set

a daily transaction limit or

notification threshold for UPI payments.

Set a notification for cumulative

UPI spends above ₹300/day

on food and groceries.

The notification creates the

friction that UPI removed —

a moment of awareness before

the next transaction.

2. Use a separate UPI-linked account

for daily groceries:

Maintain a zero-balance savings account

(Kotak 811 or ICICI iSave —

both free) linked to a separate

UPI handle used only for groceries.

Transfer your weekly grocery budget

to this account every Monday.

When it's empty, the week is done.

The visual depletion of a dedicated

account recreates the wallet-thinning

signal that cash spending provided.

3. Apply a 10-minute rule

for unplanned purchases above ₹50:

Before scanning for any unplanned

purchase above ₹50, wait 10 minutes.

This doesn't prevent the purchase —

it simply restores the decision

timeline that UPI eliminated.

For genuinely needed items,

10 minutes changes nothing.

For impulse items, 10 minutes

frequently eliminates the desire entirely.

4. Make a daily grocery list

— even for micro-purchases:

Before leaving home each morning,

spend 2 minutes writing down

any fresh produce you need that day.

Buy only those items from street vendors.

The list is not a restriction —

it's a decision made with a clear head

rather than in the moment of temptation.

5. Batch your vegetable purchases

to 3x per week instead of daily:

Daily vegetable vendor stops are

the highest-frequency unplanned

purchase trigger in most households.

Shifting to Monday–Wednesday–Friday

vegetable shopping reduces the

number of micro-purchase opportunities

by approximately 57% while maintaining

fresh produce supply.

6. Track grocery expenses

by category weekly, not monthly:

Monthly tracking catches the damage

after it's done. Weekly tracking

catches it on day 8 when you

still have 22 days to adjust.

More importantly, seeing "you've

already spent ₹2,100 in 8 days

on a ₹8,000 monthly grocery budget"

creates the same psychological

friction that an empty wallet creates.

7. Keep a physical ₹500 note

in your wallet for daily purchases:

This sounds counterintuitive but works

for specific people: using cash

for street vendor and daily micro-purchases

while using UPI for planned

supermarket shopping. The physical

note depletes visibly through the day,

recreating the spending awareness

that UPI has eliminated for daily purchases.

8. Use expense tracking Google Sheet

for weekly grocery review:

A simple Google Sheet with one row

per grocery transaction, updated

every evening, gives you a running

total that the UPI transaction history

doesn't organise for you.

The UPI app shows you individual

transactions — the sheet shows you

the monthly pattern.

Pattern visibility is what changes behaviour.

9. Set up a "grocery surplus fund":

When you come in under your

weekly grocery budget, transfer

the surplus to a separate savings

account immediately — don't let it

remain in the grocery account.

This creates positive feedback

for under-spending rather than

just negative feedback for over-spending.

The visible accumulation of the

surplus fund is motivating in a way

that budget adherence alone is not.

10. Review your UPI transaction

history every Sunday:

Open your PhonePe, Google Pay,

or BHIM transaction history

and review every grocery-related

transaction from the past week.

Categorise them as planned vs unplanned.

Calculate your impulse-to-planned ratio.

For most people, this exercise alone —

seeing the unplanned percentage in rupees —

is sufficient to change behaviour

the following week without

any other intervention.

How to Track Expenses Without Spending More Time Than the Money Is Worth

How to Track Expenses — The Methods

The biggest objection to expense tracking is time. "I can't log every ₹20 chai."

This objection is valid for complex systems. For the simple system required to counter the ₹20 trap, the time investment is 3–5 minutes per day — less than the time wasted looking at your balance and wondering where the money went.

Method 1 — UPI transaction history review: All major UPI apps maintain a complete transaction history. The data already exists — you don't need to enter anything. The gap is organisation and categorisation of that data, not its capture.

Method 2 — Expense tracking Google Sheet: A simple spreadsheet with Date, Amount, Category (Planned Grocery / Unplanned Food / Household) columns. Update once per evening from UPI history. 5 minutes daily. Gives weekly totals automatically. Free, always accessible, shareable with spouse.

Method 3 — Dedicated Indian expense tracking app (recommended for families): An app built for Indian spending patterns — with UPI-aligned categories, household budget views, and real-time running totals — removes the organisation step that makes the Google Sheet feel like work. The best budgeting apps india for this specific use case are those that show your grocery category running total against budget in real time — so you know on day 15 whether you're on pace, not on day 31.

The Real Cost of Ignoring This — Annual Numbers

The ₹20 trap is not a minor inconvenience. At scale, across a full year, the numbers are significant:

- ₹2,710/month in untracked

micro-transaction grocery overspend:

₹32,520 per year - At 12% annual return in a Nifty 50 index fund SIP, ₹32,520/year over 10 years = approximately ₹6.3 lakh in forgone investment growth

- Over 20 years at the same return: approximately ₹26 lakh

The ₹20 chai is not ₹20. Over 20 years, with the opportunity cost of investing that money instead, it is closer to ₹1,400 in forgone wealth.

This is not an argument to never buy chai. It is an argument to buy it consciously, track it honestly, and understand what the accumulated pattern costs over a lifetime.

Where RozHisab Fits Into This

The ₹20 trap is a data problem before it is a willpower problem. You cannot make better decisions about spending you cannot see.

Most Indians check their bank balance. They do not track their spending pattern — the category breakdown, the planned vs unplanned ratio, the week-on-week trend that reveals whether behaviour is improving or deteriorating.

RozHisab is built for exactly this — track every grocery expense by category, see your weekly and monthly totals against your house monthly budget, and watch your planned vs unplanned grocery ratio improve as visibility creates accountability.

No bank account linking required. Log transactions as they happen or in a 3-minute evening batch from your UPI history. See your grocery expenses, your food spending, and your total household budget in one clear dashboard — free, built for Indian households, no subscription required.

Visibility is the intervention. Tracking is the habit. The ₹20 trap closes itself the moment you can see it clearly.

👉 Start tracking your grocery expenses for free at RozHisab — log every scan and pay, see your monthly grocery pattern, and finally understand where your food budget actually goes.

Quick Reference — The ₹20 Trap Cheatsheet

- 📱 Why UPI enables impulse buying: 8-second transactions with zero physical friction — compared to 22–30 seconds for cash

- 💸 The hidden monthly cost: ₹2,500–₹3,500/month in untracked micro-transactions for most urban Indian households

- 🧠 Impulse buying behaviour fix: 10-minute rule for unplanned purchases, daily grocery list, batch vegetable shopping

- 📊 Best tracking method: Dedicated expense app with Indian grocery categories and weekly budget running total

- 📋 Family budget template: Split groceries into 4 lines — planned shop, daily fresh produce, food outside, kirana impulse

- 🔢 Annual opportunity cost: ₹32,520/year in untracked grocery overspend = ₹26 lakh forgone over 20 years at 12% return

- ✅ Top action today: Open UPI history, categorise last week's grocery transactions as planned vs unplanned — see your ratio for the first time

- 📱 Track it all: RozHisab — free, Indian-focused, no bank linking, real-time grocery budget tracking

📌 Disclaimer: This article is for educational and informational purposes only. All spending estimates, budget figures, and investment projections are illustrative only. Individual spending patterns vary significantly. The psychological research references are generalised summaries, not clinical citations. RozHisab is a budgeting and expense tracking tool — not a financial advisory service.

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →