Most Indians don't realise they're paying a hidden tax on their own money every single month.

It's called the minimum balance penalty. Miss the minimum balance requirement on a regular savings account — ₹5,000 in SBI, ₹10,000 in HDFC, ₹25,000 in some private banks — and you get charged ₹200–₹600 per quarter. Automatically. Without a reminder.

In 2026, there is absolutely no reason to pay this penalty. India now has dozens of fully-featured zero balance savings accounts — from PSU giants like SBI to private banks like ICICI and Kotak, to post offices, to digital neobanks — all offering free accounts with UPI, internet banking, and competitive interest rates with zero minimum balance requirement.

This guide compares every major option — interest rates, features, cash deposit limits, student accounts, salary accounts, and the new neobank alternatives — so you can open the right one in under 10 minutes.

What Is a Zero Balance Account?

A zero balance account is a savings account where the bank does not require you to maintain any minimum monthly average balance. You can have ₹0 in the account on any given day and no penalty will be charged.

This is different from a regular savings account where maintaining a minimum balance of ₹1,000–₹25,000 (depending on bank and branch type) is mandatory — and failure to maintain it results in quarterly penalty deductions.

Who needs a zero balance account:

- Students with irregular income or pocket money

- Fresh graduates and first jobbers whose salary hasn't started yet

- Salaried employees who want a secondary account for specific purposes (expense tracking, emergency fund) without minimum balance pressure

- Freelancers and gig workers with variable monthly income

- Anyone who has been charged minimum balance penalties and wants to stop that immediately

- People opening a zero balance account online for the first time without visiting a branch

Current Account vs Savings Account — Key Difference Before You Choose

Before comparing zero balance options, understand what type of account you actually need:

Savings Account:

Designed for personal use —

storing salary, personal savings, household expenses.

Earns interest (2.7%–7.5% depending on bank).

Has transaction limits (typically 3–5 free

cash withdrawals per month from non-home

branches). This is what 95% of individuals need.

Current Account:

Designed for business use —

high-volume daily transactions, no transaction

limits, no interest earned, higher minimum balance

requirement (typically ₹10,000–₹1 lakh).

Needed by traders, shopkeepers, and businesses

that process hundreds of transactions monthly.

If you are an individual — salaried, student, freelancer, or homemaker — you need a savings account, not a current account. Zero balance savings accounts are what this guide covers.

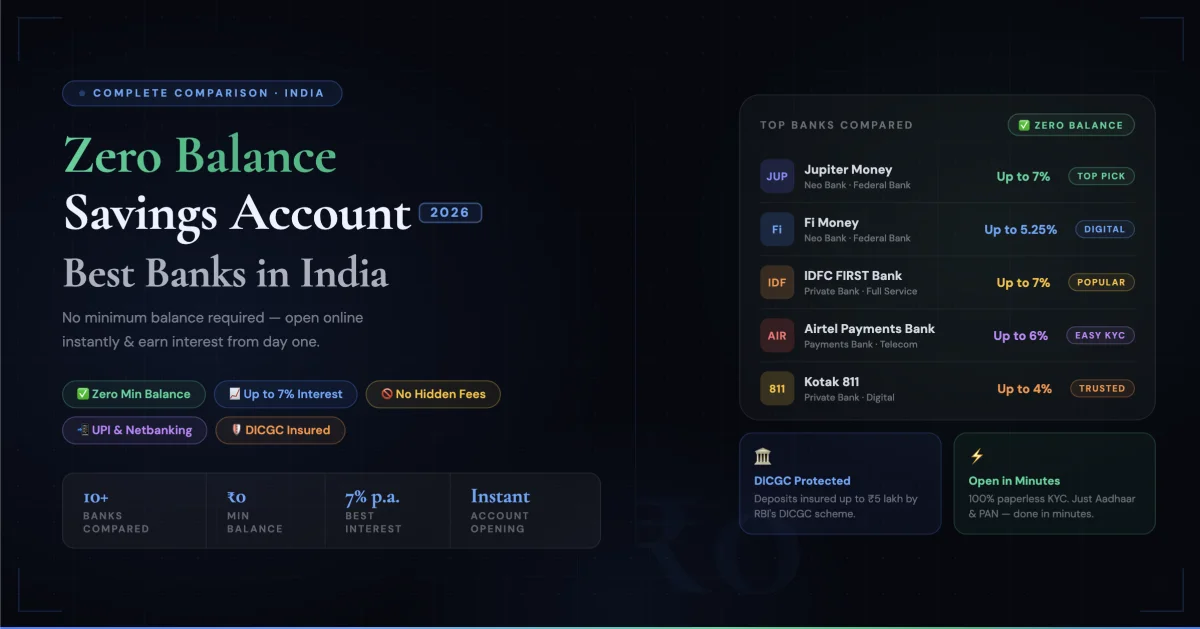

Best Zero Balance Account Opening Online — Complete Bank Comparison 2026

1. ICICI Zero Balance Account — iSave / Basic Savings Account

Interest Rate: 3.0% per annum

(balance below ₹50 lakh)

Minimum Balance: Zero

Account Opening: Fully online

via iMobile app or ICICI website —

video KYC, no branch visit required

Time to open: 15–30 minutes

Key features:

- Free UPI, IMPS, NEFT, RTGS

- Free debit card (virtual immediately, physical delivered in 5–7 working days)

- Full internet banking and iMobile app access

- Free passbook and e-statements

- 4 free ATM withdrawals per month (at ICICI ATMs) — charges apply beyond this

ICICI Zero Balance Account Opening Online — Steps:

- Download iMobile app or visit icicibank.com

- Click "Open Savings Account" → select Basic Savings Account

- Enter PAN and Aadhaar details

- Complete Video KYC (live selfie + document verification via app camera)

- Account activated — virtual debit card issued instantly

✅ Best for: People who want the reliability and network of a top private bank with zero balance flexibility. ICICI's branch and ATM network is second only to SBI in India — useful if you need in-person banking occasionally.

2. SBI Zero Balance Account Opening Online — BSBD Account

Interest Rate: 2.7% per annum

Minimum Balance: Zero

Account Opening: Online via

SBI YONO app or branch

Full name: Basic Savings Bank

Deposit (BSBD) Account

Key features:

- Free RuPay debit card

- 4 free cash withdrawals per month

- UPI and mobile banking via YONO app

- Access to India's largest bank branch and ATM network — 22,000+ branches, 65,000+ ATMs

- Government scheme linkage — PM Jan Dhan, direct benefit transfers, subsidy credits all work through SBI BSBD

Important limitation: SBI's BSBD account has restrictions — total credits cannot exceed ₹1 lakh per year and balance cannot exceed ₹50,000 at any point. If your income or savings will exceed these limits, the regular SBI savings account (with minimum balance requirement) is more appropriate.

SBI Salary Account Benefits

— A Better Zero Balance Option for Salaried:

If you're salaried, your employer may offer

an SBI salary account — which is effectively

a zero balance account with no transaction

restrictions as long as your salary

is credited monthly. SBI salary account benefits

include free unlimited ATM withdrawals,

free demand drafts, and personal accident

insurance cover. Check with your HR if

SBI is an option at your company.

✅ Best for: Rural and semi-urban users who need the widest physical branch access in India. Government employees and beneficiaries of direct benefit transfer schemes. People whose employers use SBI for salary credit.

3. Kotak 811 Zero Balance Account — Best Digital Zero Balance Account

Interest Rate: Up to 4% per annum —

highest among major bank zero balance accounts

Minimum Balance: Zero

Account Opening: Fully digital,

video KYC, opens in under 5 minutes

Named after: 8/11 —

the date of demonetisation in 2016,

when Kotak launched this as a digital-first account

Key features:

- 4% interest on balance up to ₹1 lakh — significantly better than SBI (2.7%) and ICICI (3%)

- Free virtual debit card instantly on opening

- Unlimited free UPI transactions

- Free IMPS, NEFT, RTGS via app

- Kotak 811 can be upgraded to full KYC account at branch for higher transaction limits

- Used as base for Kotak 811 #DreamDifferent Credit Card — the only major zero-fee credit card requiring no income proof

⚠️ Limitation before full KYC: Without completing full KYC at a Kotak branch, the 811 account has a total balance limit of ₹1 lakh and annual credit limit of ₹2 lakh. Complete full KYC within 12 months to remove all restrictions.

✅ Best for: Students, young professionals, and anyone who wants the best interest rate in a zero balance account with instant digital opening. Also the best option for getting a zero-fee credit card simultaneously.

4. Yes Bank Zero Balance Account

Interest Rate: Up to

6.25% per annum on higher balances

Minimum Balance: Zero

(for digital savings account variant)

Account Opening: Online via

Yes Bank app or website with video KYC

Key features:

- One of the highest interest rates among major bank zero balance accounts

- Free virtual and physical debit card

- Full UPI and mobile banking access

- Yes PayNow UPI app integration

⚠️ Consideration: Yes Bank underwent RBI-supervised restructuring in 2020. The bank has since stabilised and is operating normally — but deposits above ₹5 lakh (the DICGC insurance limit) carry slightly higher perceived risk than SBI or HDFC. For a zero balance account where you're parking ₹5,000–₹50,000, this is not a meaningful concern.

✅ Best for: Users who want a higher interest rate than Kotak 811 and are comfortable with Yes Bank's current standing.

5. Post Office Savings Account — Most Underrated Zero Balance Option

Post Office Savings Account

Interest Rate: 4.0% per annum

— government-guaranteed, unchanged for years

Minimum Balance: ₹500

(not zero — but the lowest among

non-digital options and fully government-backed)

Account Opening:

At any of India's 1.6 lakh post offices

Key features:

- Sovereign guarantee — backed by Government of India directly, no deposit insurance limit applies

- 4% interest — better than SBI and ICICI

- CBS (Core Banking Solution) enabled — accessible at any post office nationally

- Internet banking and mobile banking available (India Post Payments Bank linkage)

- Ideal base account for PPF, NSC, and other post office savings schemes

✅ Best for: Rural users, senior citizens, and anyone who wants absolute government-backed safety with competitive interest. India's most trusted savings institution for generations — and still one of the best interest rates for a near-zero balance account.

Cash Deposit Limit in Savings Account — What You Must Know

This is one of the most searched questions alongside zero balance accounts — and one of the least clearly explained. Here is the complete picture:

Cash Deposit Limit Savings Account — Income Tax Rules 2026

There is no legal upper limit on how much cash you can deposit in a savings account in India. However, the Income Tax Department monitors large cash deposits through Annual Information Statement (AIS) reporting by banks:

₹10 lakh threshold — annual reporting:

If total cash deposits in a savings account

exceed ₹10 lakh in a single

financial year, the bank is required

to report this to the Income Tax Department.

This is not illegal — but it will trigger

scrutiny if your declared income doesn't

explain the source of the cash.

₹50,000 threshold — PAN requirement:

Any single cash deposit of ₹50,000

or more requires you to provide

your PAN card details at the bank counter.

Without PAN, the bank cannot accept

the cash deposit.

Savings account deposit limit — practical rules:

- Cash deposits under ₹50,000 in a single transaction — no PAN required, no reporting

- Cash deposits above ₹50,000 — PAN mandatory

- Total cash deposits above ₹10 lakh/year — reported to IT department automatically

- Cash deposits that don't match declared income — can trigger IT notice and scrutiny

⚠️ Important for zero balance account holders: The BSBD (zero balance) accounts at SBI have an additional restriction — total credits cannot exceed ₹1 lakh/year. This is a bank-imposed limit, not an IT limit. If you regularly deposit more, upgrade to a regular savings account.

Saving account limit —

the simple rule:

Keep your cash deposits below ₹10 lakh annually

and ensure any deposits above ₹50,000

come with PAN. Keep records of the source

of any large cash — salary withdrawals,

property sales, gifts — so you can explain

them if ever asked.

Zero Balance Student Account Opening Online

Students have some of the best zero balance account options in India — specifically designed for people with no income proof.

Best Student Account Opening Zero Balance Options 2026

1. SBI Student Savings Account

Minimum Balance: Zero for students

Age: 10 years and above

Documents: Aadhaar, school/college

ID, passport photo

Features: Free RuPay card, internet banking,

YONO app access, no minimum balance

until age 21 or graduation

2. ICICI Student Account

Minimum Balance: Zero

Features: Video KYC opening,

iMobile access, virtual debit card instantly,

free UPI — can be upgraded to regular

account after graduation

3. Kotak 811 (for students 18+)

The easiest student zero balance account opening

online for college students —

no income proof, no guardian requirement,

opens in 5 minutes via app with

4% interest rate.

4. Bank Account for Students

Under 18 in India:

For students below 18, most banks require

a joint account with a parent or guardian.

SBI's Pehli Udaan and Pehla Kadam accounts

are specifically designed for minors —

with age-appropriate debit card limits

(₹5,000/day for Pehla Kadam) and

zero minimum balance.

Online Student Bank Account Opening With Zero Balance — Documents Needed:

- Aadhaar card (mandatory for KYC)

- PAN card (or Form 60 if no PAN)

- College/school ID or fee receipt (for student-specific accounts)

- Mobile number linked to Aadhaar (for OTP verification)

- Passport-size photograph (uploaded digitally for online opening)

✅ Best student zero balance account overall: Kotak 811 for students 18+ (instant digital opening, 4% interest, no income proof). SBI Pehla Kadam for students under 18 (parental joint account, zero balance, government-backed).

Salary Account as Zero Balance Account — Everything You Need to Know

If you are salaried, your salary account is already effectively a zero balance account — as long as your salary is credited every month.

Salary accounts at all major Indian banks (SBI, HDFC, ICICI, Axis, Kotak) come with zero minimum balance requirement — the bank waives the minimum balance condition because your employer has an arrangement with the bank for bulk salary credits.

SBI Salary Account Benefits:

- Zero minimum balance as long as salary credited monthly

- Unlimited free ATM withdrawals at SBI ATMs (and 5 free at other bank ATMs)

- Free demand drafts and pay orders

- Personal accident insurance cover (₹2 lakh for PMJJBY-linked accounts)

- Overdraft facility up to 2 months salary

- Free multi-city cheque book

Axis Salary Account:

Axis Bank is a popular salary account

choice for private sector companies —

particularly in IT, BFSI, and manufacturing.

Axis salary account offers zero balance,

free unlimited Axis ATM withdrawals,

EDGE rewards points on debit card spends,

and priority customer service.

ICICI Bank Salary Account:

ICICI's salary account (iSalary) comes with

zero balance, instant credit of salary,

free IMPS/NEFT/RTGS,

and preferential rates on home and

personal loans — useful when you apply

for credit later.

⚠️ Important: If you leave a job and salary stops being credited, your salary account converts to a regular savings account — minimum balance rules apply from the next month. Either close it, convert it to a zero balance account, or transfer your banking to your new employer's salary account immediately.

Neobanks in India — The New Alternative to Traditional Zero Balance Accounts

What Is a Neobank?

A neobank is a fully digital bank that operates without physical branches, offering banking services entirely through a mobile app. In India, neobanks typically partner with RBI-licensed banks to offer savings accounts — they provide the app and experience, the partner bank holds the actual deposits.

All neobank deposits in India are held with RBI-licensed partner banks and are protected by DICGC insurance up to ₹5 lakh — the same protection as any other bank account.

Major Neobanks in India 2026:

Jupiter — Partners with Federal Bank. Offers zero balance account, 3% interest, smart spend analytics, automatic savings "Pots" feature, and a well-designed budgeting interface. Best neobank for expense tracking alongside banking.

Fi Money — Partners with Federal Bank. Targeted at salaried professionals — salary account with zero balance, smart savings features, "Jars" for goal-based savings, and built-in investment options (mutual funds, US stocks). Best neobank for salaried tech professionals.

Niyo — Partners with SBM Bank India. Particularly known for zero forex markup on international transactions — making it the best travel account for Indians going abroad.

Freo — Offers a zero balance savings account plus a buy-now-pay-later credit line. Useful for young users building a credit history.

Neobank vs Traditional Bank — Quick Comparison:

- 🏦 Traditional bank (SBI/ICICI/Kotak): Physical branches, ATM network, established trust, full banking services, potentially slower app experience

- 📱 Neobank (Jupiter/Fi): Superior app experience, better budgeting tools, faster customer service via chat, no physical branch access, newer institutions with shorter track records

✅ Best for: Tech-savvy millennials and Gen Z who do all banking on their phone and want built-in budgeting and savings analytics. Not ideal as a primary account for people who need occasional branch or cash services.

How to Open a Zero Balance Account Online — Step by Step (Any Bank)

The online bank account opening with zero balance process is now standardised across all major Indian banks thanks to RBI's Video KYC guidelines. Here is the general process:

What you need before starting:

- ✅ Aadhaar number + mobile number linked to Aadhaar (for OTP)

- ✅ PAN card number

- ✅ Smartphone with front camera (for video KYC selfie)

- ✅ White paper and pen (some banks ask you to write today's date on paper and hold it during video KYC)

- ✅ Good lighting and stable internet connection

General steps for online zero balance account opening:

- Download the bank's app or visit their website

- Click "Open Account" → select Savings / Zero Balance account

- Enter mobile number → receive and verify OTP

- Enter PAN details → enter Aadhaar number → complete Aadhaar OTP verification

- Fill in personal details (name auto-fetched from Aadhaar)

- Complete Video KYC — a bank official connects via video call, verifies your face, and asks you to show your PAN card on camera

- Account number generated — virtual debit card issued immediately

- Physical debit card dispatched to your address in 5–7 working days

Total time: 10–30 minutes for most banks. Kotak 811 is fastest at under 5 minutes for full opening.

Best Zero Balance Account — Quick Comparison Table

- 🏆 Best interest rate: Yes Bank (up to 6.25%) → Kotak 811 (4%) → Post Office (4%)

- ⚡ Fastest to open: Kotak 811 (under 5 minutes, fully digital)

- 🌐 Widest branch network: SBI (22,000+ branches, 65,000+ ATMs)

- 👩🎓 Best for students (18+): Kotak 811 (no income proof, instant opening, 4% interest)

- 👦 Best for students under 18: SBI Pehla Kadam (parental joint account, government-backed)

- 💼 Best salary account (zero balance): Axis or ICICI salary account (depends on employer tie-up)

- 🏛️ Safest (government-backed): Post Office Savings Account (sovereign guarantee, no DICGC limit)

- 📱 Best neobank option: Jupiter or Fi Money (superior app, built-in expense analytics)

- ✈️ Best for international travel: Niyo (zero forex markup)

- 🔗 Best for getting a credit card too: Kotak 811 (base for Kotak 811 #DreamDifferent Credit Card — no income proof needed)

Track Your Zero Balance Account Alongside All Your Finances

Opening the right zero balance account is step one. Step two — the step most people skip — is actually knowing what's happening in that account every month.

Most Indians with multiple bank accounts (salary account + secondary zero balance account + family joint account) have no clear picture of their total liquid balance, total monthly spending, or actual savings rate across all accounts combined.

They log into three separate apps, see three separate balances, and still don't know their complete financial position.

Use RozHisab to track all your bank accounts — zero balance, salary, savings — alongside every expense and income in one place. See your total balance, monthly cash flow, and savings rate across all accounts in a single dashboard. Completely free, no ads, built specifically for Indian households.

Because a zero balance account with zero financial visibility is still a step backward. The goal is zero balance penalty AND complete money clarity.

👉 Start tracking all your accounts for free at RozHisab — open your zero balance account today, track it on RozHisab tomorrow, and finally know exactly where every rupee is going.

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →