ℹ️ Disclaimer: This article is for general educational and informational purposes only. Stamp duty rates, registration charges, GST slabs, property tax, maintenance charges, and legal fees vary by state, city, property type, and change periodically. All figures and examples are illustrative only. Please consult your builder, lawyer, or a qualified financial advisor before making any property purchase decision. RozHisab is a personal finance tracking tool — not a legal or real estate advisory service.

You spend months shortlisting properties. You negotiate hard and get the seller down ₹3 lakh from the asking price. You feel good about the deal.

Then the paperwork begins — and you discover that the ₹3 lakh you saved in negotiation doesn't even cover the stamp duty on the transaction.

This is the reality of home buying in India. The quoted price of a property — the number on the brochure, the number you negotiated, the number your home loan is based on — is not what you will actually pay.

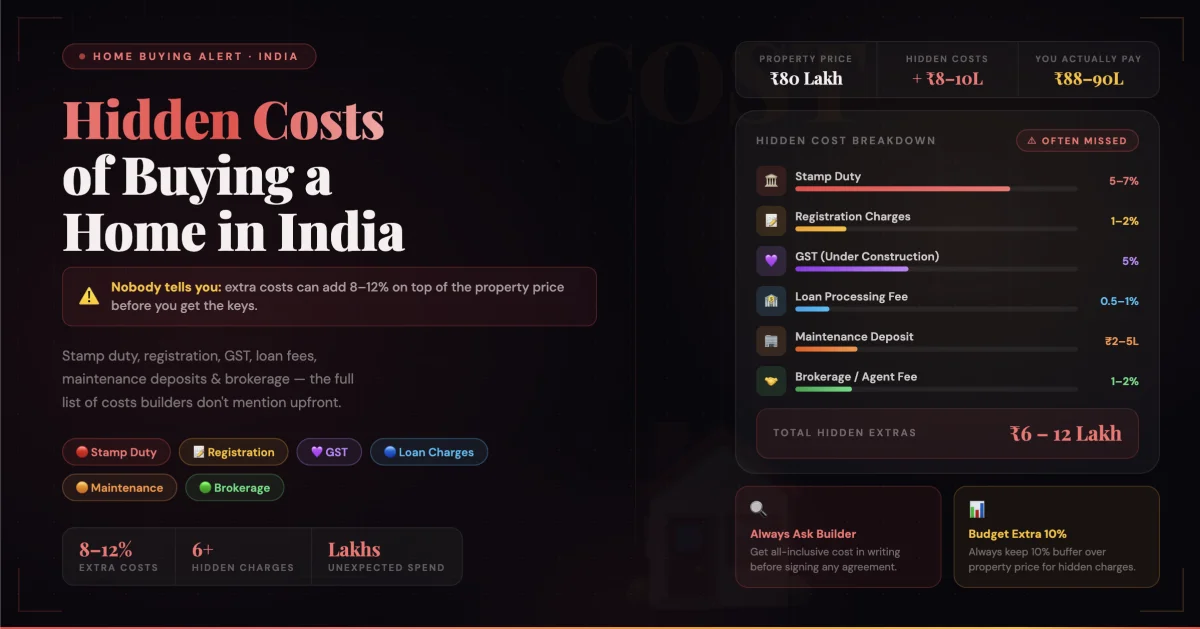

The true cost of buying a home in India is 10–25% higher than the property's sale price, depending on location, property type, and how you choose to furnish it. Most first-time buyers discover this gap after they've already signed on the dotted line.

This guide lays out every hidden cost — with real numbers — so there are no surprises.

The Complete List of Hidden Costs When Buying a Home in India

Here is every cost beyond the property's sale price that a buyer in India typically pays:

- Stamp duty

- Property registration charges

- GST (for under-construction properties)

- Home loan processing fee and insurance

- Legal charges and documentation fees

- Mutation charges

- Property tax (ongoing)

- Annual maintenance charges and corpus fund

- Interior design and fit-out costs

- Brokerage fees

Walk through each one below — with what it is, how much it costs, and what most buyers miss.

1. Stamp Duty — The Biggest Hidden Cost Nobody Calculates Early Enough

What is stamp duty?

Stamp duty is a state government tax paid on the legal transfer of property from seller to buyer. It is the fee you pay for the government to officially recognise you as the new owner of the property. No stamp duty payment = no legal ownership transfer.

What is stamp duty value of property? Stamp duty is calculated on the higher of two values: the actual transaction price (what you paid) OR the circle rate / ready reckoner rate set by the state government for that area. If you buy a flat for ₹80 lakh but the government's circle rate values it at ₹90 lakh, stamp duty is charged on ₹90 lakh — not ₹80 lakh.

What is stamp duty and registration charges — state-wise rates (illustrative):

Maharashtra: 5% stamp duty + 1% registration charge (reduced rates for women buyers in some cases)

Karnataka: 5% stamp duty on properties above ₹45 lakh; 3% on ₹21–45 lakh; 2% below ₹21 lakh + 1% registration charge

Delhi: 6% for men, 4% for women + 1% registration

Uttar Pradesh: 7% stamp duty + 1% registration

Tamil Nadu: 7% stamp duty + 4% registration

⚠️ Stamp duty and registration charges calculator —

a real example:

Property price: ₹75 lakh in Maharashtra

Stamp duty (5%): ₹3,75,000

Registration charge (1%): ₹75,000

Total: ₹4,50,000 — in cash, upfront,

before you get the keys.

Most banks do not include stamp duty and registration in the home loan amount. You pay this from your own pocket on or before the registration date.

Can I pay stamp duty with a credit card?

No — in most states, stamp duty cannot be paid with a credit card. Stamp duty in India is paid via e-franking, franking machine, or online payment through the state government's portal (GRAS in Maharashtra, IGRS in Telangana and Andhra Pradesh, KAVERI in Karnataka, etc.). These portals typically accept net banking and UPI — not credit cards. A few states may accept debit cards on specific portals, but credit card payment for stamp duty is generally not supported. Verify with your sub-registrar office or the builder's documentation team.

How to pay stamp duty online:

- Visit your state's IGRS or GRAS portal

- Select property registration / stamp duty payment

- Enter property details, buyer/seller info, and transaction value

- Pay online via net banking or UPI

- Download the e-challan / receipt

- Carry this for the sub-registrar appointment

Some states require physical franking at designated banks — your builder's documentation team will guide you on the specific process for your state.

2. GST on Property Purchase

GST on under-construction property:

GST applies only to under-construction properties. Completed, ready-to-move properties with an Occupancy Certificate (OC) do NOT attract GST — this is one of the main financial advantages of buying ready-to-move.

GST on under-construction property rate:

- Affordable housing (carpet area ≤ 60 sqm in metros, ≤ 90 sqm in non-metros, price ≤ ₹45 lakh): 1% GST (no ITC)

- Other residential properties: 5% GST (no ITC)

GST on residential property example:

Under-construction flat worth ₹80 lakh

(non-affordable category):

GST at 5% = ₹4,00,000 extra

On top of stamp duty already calculated above,

this adds another ₹4 lakh to your

out-of-pocket expenses before possession.

GST on commercial property: Commercial properties attract 18% GST on rent and 12% GST on purchase of under-construction commercial space — significantly higher than residential rates. If you're buying a commercial shop or office, factor this in separately.

GST on property — what's not applicable: No GST on land purchases, no GST on resale transactions (flat bought from another individual), no GST on ready-to-move flats with OC. The GST applies to the developer-buyer transaction only for under-construction projects.

3. Home Loan Hidden Costs

How much home loan can I get on ₹40,000 salary?

Before getting to the hidden loan costs, a quick benchmark most first-time buyers ask: On a ₹40,000/month net salary, you can typically get a home loan of ₹18–22 lakh based on the standard 40–50% EMI-to-income ratio that most banks apply. On ₹60,000/month net salary, the range is ₹27–33 lakh. These are rough estimates — actual eligibility depends on credit score, existing EMIs, age, and lender policy.

The hidden costs within the loan itself:

Processing fee:

Most banks charge 0.25–1% of the loan amount as a one-time processing fee when you apply for the home loan. On a ₹50 lakh loan, this is ₹12,500–₹50,000 — non-refundable even if the loan is rejected.

Is home loan insurance mandatory?

No — home loan insurance is not mandatory by law. Banks and NBFCs are not legally permitted to force you to buy home loan insurance (also called home loan protection plan or HLPP) as a condition for loan approval. However, many banks strongly push it and some make it appear mandatory during the sales process.

Is insurance compulsory for home loan? The RBI has clarified that banks cannot make the purchase of any insurance product a condition for loan approval. You have the right to refuse HLPP or buy it from any insurer of your choice — not only the one the bank recommends.

Is insurance mandatory for home loan? Legally no — but practically, evaluate it. If you have dependents and your income is the sole source of EMI payments, a term insurance plan covering the loan outstanding makes sense. A standalone term plan is usually significantly cheaper than the bundled HLPP that banks sell, which is typically a single-premium plan added to the loan amount (meaning you pay interest on insurance too).

Other loan costs:

- Legal/technical verification fee: ₹3,000–₹10,000 (bank sends a lawyer and valuer to verify the property — you pay for both)

- MODT (Memorandum of Deposit of Title Deed): 0.1–0.3% of loan amount in some states

- Franking charges on loan agreement: ₹500–₹5,000 depending on state

4. Legal Charges — The Cost of Documentation Nobody Budgets For

Legal charges meaning:

Legal charges in property transactions refer to the fees paid to lawyers, notaries, and documentation specialists for verifying title, preparing sale agreements, reviewing builder agreements, and handling the sub-registrar registration process.

Legal charge components in a property purchase:

- Title search and verification: ₹5,000–₹25,000 — a lawyer checks that the seller has clear, undisputed title and the property has no encumbrances, disputes, or liens. Never skip this.

- Sale agreement drafting: ₹3,000–₹15,000

- Registration assistance: ₹2,000–₹10,000 for the sub-registrar visit, document preparation, and follow-up

- Notary charges: ₹500–₹2,000 for various affidavits required during registration

Total legal charges range: ₹15,000–₹60,000 for a typical residential property purchase. Builders often recommend their panel lawyers — you are not obligated to use them and can hire your own independent lawyer.

5. What is Mutation of Property — The Step Everyone Forgets After Registration

What is mutation of property?

Mutation of property is the process of updating government revenue records (the land records / khata / property register) to reflect the new owner's name after a property purchase or transfer. Registration at the sub-registrar's office transfers legal ownership — but the municipal revenue records still show the previous owner's name until mutation is done.

What is mutation of land?

Mutation of land specifically refers to updating the land revenue register (maintained by the Tehsildar or revenue department) to reflect ownership change for a land parcel. For apartments, the equivalent is updating the khata (in Karnataka) or property assessment records with the local municipal body (BMC, BBMP, GHMC etc.).

Why mutation matters:

- Property tax is billed in the registered owner's name — if mutation isn't done, tax notices go to the previous owner, creating confusion and potential legal complications

- Future sale of the property is complicated if mutation records don't match ownership

- Required for utility connections (water, electricity) in the new owner's name in some states

Mutation charges: Typically ₹500–₹10,000 depending on state and property value. Low cost but significant administrative importance.

What is mutation in land — timeline: Apply within 3–6 months of registration. Most states now have online portals for mutation applications. Karnataka: KAVERI portal; Maharashtra: online through local municipality; Delhi: online through MCD/DDA portals.

6. Property Tax — The Ongoing Annual Cost

How to calculate property tax:

Property tax in India is levied by the local municipal body (BMC in Mumbai, BBMP in Bangalore, MCD in Delhi, GHMC in Hyderabad). It is an annual recurring expense that begins from the year of purchase.

Property tax formula (varies by municipality):

Property Tax = Annual Value × Tax Rate

where Annual Value = carpet area ×

monthly rate per sq ft × 12

How to change name in property tax: After mutation is complete, approach your local municipal body with the new sale deed, mutation certificate, and a change-of-name application. Most municipalities now allow this online. Your builder may handle this as part of the handover process for new properties.

What is assessment number in property tax? The assessment number (also called property identification number or PID) is the unique identifier assigned by the municipal body to your property for tax billing and tracking purposes. You need this number to pay property tax online, track dues, and update ownership records. For new apartments, the builder applies for the assessment number on behalf of buyers.

What is user charges in property tax? User charges are fees levied in addition to base property tax for specific municipal services — typically water supply, sewage, garbage collection. In some cities like Bangalore (BBMP), user charges are billed as a separate line item alongside the main property tax amount.

7. How to Save Property Gain Tax — Capital Gains on Future Sale

This isn't a cost today — but plan for it now.

How is capital gains tax calculated on sale of property? When you sell the property in the future, the profit (sale price minus indexed purchase cost) is subject to capital gains tax.

- Short-term capital gains (STCG): If property is sold within 2 years — gains added to income and taxed at slab rate

- Long-term capital gains (LTCG): If held more than 2 years — gains taxed at 20% with indexation benefit (indexation adjusts the purchase price for inflation using the Cost Inflation Index)

How to save property gain tax:

- Section 54: Reinvest LTCG in another residential property within 2 years (purchase) or 3 years (construction) — capital gains are exempt

- Section 54EC: Invest LTCG in specified bonds (NHAI, REC) within 6 months of sale — exemption up to ₹50 lakh

- Keep all purchase records: Stamp duty, registration charges, brokerage, legal fees, home loan interest (during construction), and interiors are all part of your indexed cost of acquisition — reducing taxable gains at the time of sale

8. Annual Maintenance Charges and Corpus Fund — The Two Costs Builders Bury in the Fine Print

What are maintenance charges?

Maintenance charges are monthly or annual fees paid to the Residents' Welfare Association (RWA) or society management for the upkeep of common areas — lifts, lobby, security, parking, garden, swimming pool, clubhouse, gym, and building maintenance.

Annual maintenance charges range: ₹2,000–₹8,000/month depending on the amenities, city, and society size. Premium gated communities in Bangalore, Pune, or Hyderabad commonly charge ₹5,000–₹15,000/month in maintenance. Budget this as a fixed monthly expense from day one of possession.

GST on apartment maintenance charges:

GST on maintenance charges is applicable when the monthly contribution to the RWA exceeds ₹7,500/month per flat. Above this threshold: 18% GST applies on the full amount (not just the amount above ₹7,500).

Example:

Monthly maintenance: ₹10,000/month

GST at 18%: ₹1,800/month

Actual monthly outflow: ₹11,800/month

Annual: ₹1,41,600 — just for maintenance

GST on maintenance charges — threshold rule: If your society's monthly maintenance is ₹7,500 or below per flat, no GST applies. Many societies structure their charges to stay at or below this threshold specifically to avoid GST applicability.

What is corpus fund?

Corpus fund meaning: A corpus fund is a one-time, non-refundable amount collected by the builder or RWA at the time of possession — set aside as a reserve fund for major future expenses: lift replacement, structural repairs, terrace waterproofing, pump replacement, and other capital expenditure the society will incur over decades.

What is corpus fund in apartments? In apartment societies, the corpus fund is collected once at handover and handed over to the newly formed Residents' Welfare Association (RWA). It is the society's financial safety net — ensuring major repairs can be done without levying a sudden large charge on all residents.

What is corpus fund in redevelopment? In redevelopment projects (older buildings being demolished and rebuilt), the corpus fund takes on added importance — existing residents negotiate a corpus fund from the developer as part of the redevelopment agreement, to be deposited in a fixed account for the society. The interest from this corpus is often used to fund ongoing maintenance during construction.

Corpus fund amount: Typically ₹25,000–₹2,00,000 per flat depending on the project size, city, and builder. This is paid at possession — the time when you're already paying stamp duty, registration, GST, and interiors simultaneously. Most buyers are caught off guard by this charge.

Is corpus fund refundable? No — corpus fund is non-refundable. When you sell the flat, the corpus fund stays with the society. (Though in practice, buyers sometimes negotiate this into the sale price informally.)

9. Interior Design and Fit-Out Costs — The Biggest Variable Nobody Budgets

The property price your home loan covers. The stamp duty you've now budgeted for. What most first-time buyers completely underestimate — or don't budget for at all — is the cost of making the flat livable.

A new flat from a builder typically comes with:

- Bare floors (vitrified tiles, sometimes)

- Bare walls (primer only)

- Basic bathroom fittings

- No kitchen — sometimes just a slab

- No wardrobes, no storage, no lighting

To make it a functional home, you need to add everything.

Drawing room interior design cost:

The living room (drawing room) is typically the highest-spend zone. A mid-range drawing room interior design in a Tier-1 city includes: false ceiling with cove lighting, feature wall, sofa, centre table, TV unit, curtains, and décor — budget ₹1,50,000–₹3,50,000 for a mid-range finish.

Hall interior design cost:

Hall and drawing room are often used interchangeably in Indian real estate. For a hall + dining area combined, mid-range hall interior design in a 2BHK runs ₹2,00,000–₹5,00,000 depending on material choices, modular vs. carpenter work, and city.

Luxury bedroom interior design cost:

A luxury bedroom interior design setup — with custom wardrobe, false ceiling, accent wall, quality bed and mattress, side tables, and lighting — runs ₹1,50,000–₹4,00,000 per bedroom in metro cities for premium finishes.

Total interior fit-out estimate for a 2BHK:

Budget ranges based on finish level:

- Basic/functional: ₹3,00,000–₹5,00,000 (standard modular kitchen, basic wardrobes, painting, flooring, lights)

- Mid-range: ₹6,00,000–₹10,00,000 (modular kitchen, custom wardrobes, false ceilings, feature walls, decent furniture)

- Premium/luxury: ₹12,00,000–₹25,00,000+ (luxury bedroom interior design, premium kitchen, high-end materials, designer lighting, custom furniture)

This is the single largest hidden cost for most home buyers — and it is entirely outside the home loan amount. Most banks will not finance interiors under a standard home loan. (A top-up loan after possession is one option — but at a higher rate.)

10. Brokerage Fees

If you buy through a broker or real estate agent, the standard brokerage fee in India is 1–2% of the property value paid by the buyer (and sometimes by the seller too — a double-sided commission).

On a ₹75 lakh flat: ₹75,000–₹1,50,000 in brokerage. This is negotiable — but often not negotiated because buyers are focused on the property price.

For new builder projects, brokerage is typically paid by the builder to the channel partner — not by you directly. Verify this upfront.

The Complete Hidden Cost Tally — A Real Example

Here is the full cost breakdown for a ₹75 lakh under-construction 2BHK flat in Pune (illustrative example):

Property price: ₹75,00,000

Add: Mandatory government charges

- Stamp duty (5% Maharashtra): ₹3,75,000

- Registration charge (1%): ₹75,000

- GST at 5% (under construction): ₹3,75,000

- Mutation charges: ₹5,000

- Government charges total: ₹8,30,000

Add: Finance and documentation

- Home loan processing fee (0.5% on ₹55 lakh loan): ₹27,500

- Legal and title verification: ₹20,000

- Bank's legal/technical fee: ₹7,500

- MODT and franking: ₹15,000

- Finance and documentation: ₹70,000

Add: At possession

- Corpus fund: ₹1,00,000

- Advance maintenance (6 months): ₹30,000

- Possession charges: ₹1,30,000

Add: Interiors (mid-range 2BHK)

- Modular kitchen, wardrobes, false ceiling, painting, furniture, lights: ₹8,00,000

Total actual cost: ₹93,30,000

Hidden costs beyond sale price: ₹18,30,000

Effective premium over quoted price: 24.4%

You budgeted ₹75 lakh. You will spend ₹93 lakh. The ₹18 lakh gap is not a surprise — it's just something nobody told you to plan for in advance.

Three Things Most Home Buyers Get Wrong About Hidden Costs

1. Assuming the home loan covers everything:

It doesn't. Stamp duty, GST,

registration, corpus fund, interiors,

and brokerage are all outside the loan.

You need liquid savings of at least

10–15% of the property value

beyond the down payment — just for these costs.

2. Not checking the circle rate

before finalising the property price:

If the circle rate is higher than

your agreed price, stamp duty is

calculated on the circle rate — not your deal.

This changes your stamp duty outflow significantly.

Check the applicable circle rate

on your state's IGRS website before signing.

3. Not budgeting for interiors

before taking possession:

Possession happens and you scramble

to get the flat ready quickly —

which means rushed decisions and

overpaying interior contractors.

Engage an interior designer 4–6 months

before possession, get proper quotes,

and have the money ready.

The drawing room interior design,

hall interior design, bedroom interiors,

and kitchen together can easily cross

₹8–12 lakh for a mid-range 2BHK.

Track Every Rupee of Your Home Purchase — From Down Payment to Monthly Maintenance

A home purchase is the largest financial transaction most Indian families will ever make. And unlike a salary, which is a single monthly credit — a home purchase is dozens of separate payments over 12–18 months: down payment, GST tranches, stamp duty, registration, corpus fund, interiors in phases, first-year maintenance.

Most buyers track none of this systematically. They lose receipts, underestimate spending, and don't know their actual total outflow until the credit card bill arrives.

Use RozHisab to log every home-related payment as it happens — tag them as "Home Purchase" and see the running total of what you've actually spent beyond the quoted property price. When the loan EMI starts, you'll also be tracking it alongside monthly maintenance, property tax, and interiors in progress — giving you the complete picture of what homeownership is actually costing you.

Because understanding hidden costs before you buy is the first step. Tracking them after you've bought is what keeps your finances from going off track during the most cash-intensive period of your financial life.

👉 Start tracking your home purchase expenses for free at RozHisab — built for Indian households managing every rupee of a major purchase.

Quick Reference — Every Hidden Home Buying Cost at a Glance

- 🏛️ What is stamp duty: State government tax on property transfer. 4–8% of property value depending on state. Paid in cash before registration — not covered by home loan.

- 📋 GST on property purchase: 5% on under-construction properties, 1% for affordable housing. Zero GST on ready-to-move with OC.

- 🏦 Is home loan insurance mandatory: No — legally not required. Evaluate standalone term insurance instead of bundled HLPP.

- ⚖️ Legal charges meaning: Title verification, sale deed drafting, registration assistance. Budget ₹15,000–₹60,000.

- 📝 What is mutation of property: Updating revenue records to your name after registration. Low cost, high importance. Do it within 3–6 months of registration.

- 💰 What is corpus fund: One-time non-refundable reserve fund paid at possession. ₹25,000–₹2 lakh. Goes to the society — not refundable on sale.

- 🏢 GST on apartment maintenance charges: 18% GST applies if monthly maintenance exceeds ₹7,500/flat. Plan for this in your budget.

- 🛋️ Interior design cost: ₹3–12 lakh for a 2BHK depending on finish. The single largest hidden cost most buyers don't budget for until possession day.

- 📊 How to save property gain tax: Keep all purchase receipts — stamp duty, legal fees, interiors all add to your indexed cost and reduce future taxable gains.

- 📱 Track total home purchase spend: Log on RozHisab — tag all payments and see your real total outflow beyond the property's quoted price.

📌 Disclaimer: This article is for educational and informational purposes only. Stamp duty rates, registration charges, GST slabs, property tax, corpus fund norms, maintenance charges, and home loan insurance rules vary by state, property type, lender, and financial year — and change periodically. All figures and examples are illustrative only. Please consult your builder, lawyer, or a qualified financial advisor before making any property purchase decision. RozHisab is a budgeting and expense tracking tool — not a legal or real estate advisory service.

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →