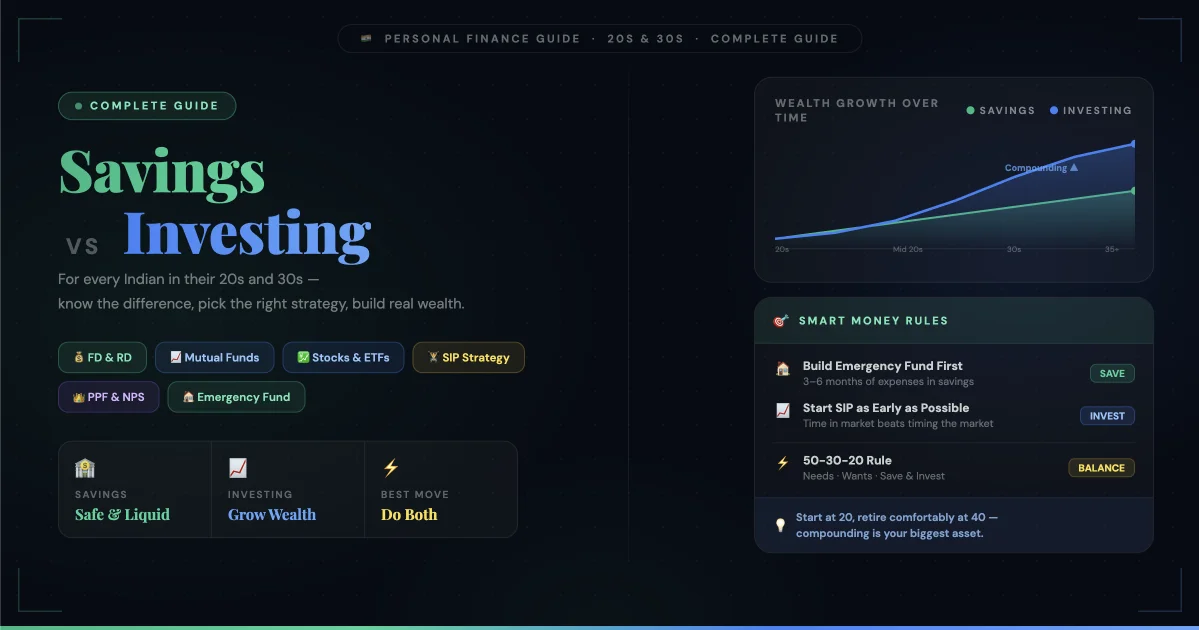

Here's a question most 25-year-olds in India never get asked:

What is the difference between saving ₹10,000 per month and

investing ₹10,000 per month — over 30 years?

Saving in a bank savings account at 3.5% interest:

Your ₹10,000/month becomes approximately ₹63 lakh by age 55.

Investing in a diversified equity mutual fund at 12% average

annual return: Your ₹10,000/month becomes approximately

₹3.5 crore by age 55.

Same amount of money. Same 30 years. A difference of nearly

₹3 crore — created entirely by the choice of where to put it.

This article covers everything: what a savings account is and

when it makes sense, what fixed deposits and RBI bonds are,

how to start investing in mutual funds, stocks, US stocks,

real estate, and green energy — even on a ₹30,000/month salary.

No jargon. No assumptions. Just the complete picture.

Part 1 — Savings: What It Is, Where to Keep It, and What It's Actually For

What Is a Savings Account?

A savings account is a deposit account held at a bank where you

store money that you might need in the short term. It earns interest

— currently between 2.7% and 7% per year depending on the bank —

and your money is available to withdraw anytime.

Savings accounts are not investment vehicles. They are safety nets.

The purpose of a savings account is not to grow your wealth.

It is to hold your emergency fund, your monthly operating cash,

and money you will need within the next 6–12 months.

The mistake most Indians make: keeping all their money in a

savings account because it feels safe. It is safe — but it is

also slowly losing value to inflation. If inflation is running

at 6% and your savings account gives 3.5%, you are losing

2.5% of your purchasing power every year without doing anything wrong.

How Much Cash Can Be Deposited in a Savings Account?

There is no upper limit on how much you can deposit into a

savings account in India. However, the Income Tax Department

monitors large cash deposits.

Key rules to know:

Cash deposits above ₹10 lakh in a single financial year in

one savings account must be reported by the bank to the IT

department. This is not illegal — but it will invite scrutiny

if your declared income doesn't match the deposit amount.

Cash deposits above ₹50,000 in a single transaction require

you to provide your PAN card.

For digital transfers (NEFT, IMPS, UPI) — there is no such

reporting threshold. Only cash deposits trigger these rules.

The practical takeaway: keep what you need liquid in your

savings account. Move the rest into instruments that actually

earn something.

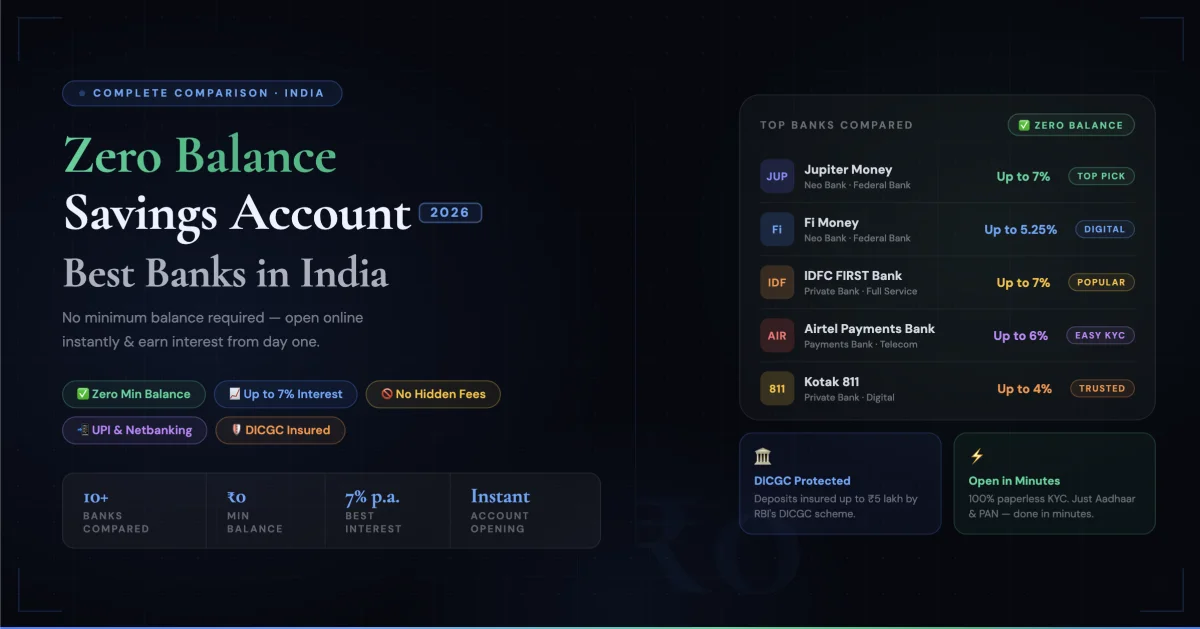

Which Bank Gives the Highest Interest Rate on Savings Account in India?

As of 2026, here is the landscape of savings account interest

rates in India:

Large PSU Banks (SBI, PNB, Bank of Baroda):

2.7% – 3.0% per year. Safe, widely accessible, but

lowest returns on savings accounts.

Large Private Banks (HDFC, ICICI, Axis, Kotak):

3.5% – 4.0% per year for regular balances.

Kotak 811 offers up to 4% with no minimum balance.

Small Finance Banks (AU Small Finance, Equitas, Jana,

Ujjivan, ESAF):

6.0% – 7.5% per year. Significantly higher than large banks.

Deposits up to ₹5 lakh are insured by DICGC — the same

government deposit insurance that covers SBI accounts.

Recommendation: For your emergency fund (3–6 months of expenses),

consider splitting between a large private bank for convenience

and a small finance bank like AU Small Finance or Equitas for

the higher interest rate. You get accessibility plus better returns

on the portion you're not touching frequently.

You can use RozHisab to track exactly how much is sitting in

each account — and whether you're holding more than you actually

need liquid, which is money that should be working harder for you.

What Is a Savings Bond?

A savings bond is a government-issued debt instrument where

you lend money to the government for a fixed period at a

guaranteed interest rate.

In India, the most relevant savings bond is the RBI Floating

Rate Savings Bond (2020), which currently pays 8.05% per year —

significantly better than most savings accounts and comparable

to fixed deposits.

Key features of RBI Bonds:

- Issued by the Reserve Bank of India — zero default risk

- Interest rate is floating, linked to NSC (National Savings Certificate) rate + 0.35%

- Minimum investment: ₹1,000

- Tenure: 7 years (with premature exit options for senior citizens)

- Interest paid semi-annually directly to your bank account

- Not tradeable on stock exchange

RBI Bonds are ideal for: conservative investors with a 7-year

horizon who want better returns than an FD without any market risk.

Parents investing for children's education. Retirees wanting

regular interest income.

Part 2 — Fixed Deposits: India's Most Popular (and Most Misunderstood) Investment

What Is a Fixed Deposit?

A Fixed Deposit (FD) is a savings instrument where you deposit

a lump sum with a bank for a fixed period — ranging from 7 days

to 10 years — at a fixed interest rate agreed at the time of deposit.

Unlike a savings account where interest can change monthly,

an FD locks in your rate for the entire tenure. This predictability

is the main appeal.

Current FD interest rates in India (2026):

SBI: 6.5% – 7.1% (general public), 7.0% – 7.6% (senior citizens)

HDFC Bank: 6.6% – 7.25%

AU Small Finance Bank: 7.25% – 8.0%

Unity Small Finance Bank: up to 9.0% for specific tenures

Tax treatment: FD interest is fully taxable as income.

If you're in the 30% tax bracket, a 7% FD is effectively

earning you 4.9% post-tax — which barely beats inflation.

What Is a Fixed Deposit Account?

A fixed deposit account is simply the account the bank opens

in your name to hold your FD. It is separate from your savings

or current account.

When you book an FD online through your bank's app or net

banking, the bank automatically creates an FD account,

debits your savings account, and issues you an FD receipt

(now digital).

You can hold multiple FDs simultaneously — a common strategy

called FD laddering, where you split your FD corpus across

different maturity dates so you always have access to some

FD money without breaking all of them.

Example: Instead of one ₹3 lakh FD for 3 years, you create:

₹1 lakh FD for 1 year

₹1 lakh FD for 2 years

₹1 lakh FD for 3 years .

This gives you liquidity every year while still earning

FD rates on the full corpus.

Part 3 — Investing: The Part That Actually Builds Wealth

Saving preserves money. Investing multiplies it.

The core difference:

Savings instruments (FD, savings account, RBI bonds) give

you fixed, predictable returns of 3–9%. They protect capital

but don't significantly grow it above inflation over time.

Investing instruments (mutual funds, stocks, real estate,

US stocks) give you variable returns — sometimes negative

in the short term — but historically 10–15% annually over

long periods in India. Over 20–30 years, this compounding

effect is transformational.

The question is not savings OR investing. The answer is

always both — savings for your emergency fund and short-term

needs, investing for everything beyond that.

Now, here's how each major investment category works.

Part 4 — Mutual Funds: The Best Starting Point for Most Indians

Types of Mutual Funds in India

A mutual fund pools money from thousands of investors and

deploys it across stocks, bonds, or other assets, managed

by a professional fund manager.

The major types:

Equity Mutual Funds: Invest primarily in stocks. Highest risk, highest long-term returns (12–15% historically over 10+ years).

Subcategories:

— Large Cap Funds: Invest in India's top 100 companies (Reliance, TCS, HDFC Bank). Most stable equity funds.

— Mid Cap Funds: Invest in companies ranked 101–250. Higher growth potential, higher volatility.

— Small Cap Funds: Companies below rank 250. Highest growth potential over a decade, but can fall 40–50% in corrections. Only for long-term investors.

— Flexi Cap / Multi Cap: Fund manager can invest across any market cap. Most flexible.

— ELSS (Equity Linked Savings Scheme): Tax-saving mutual fund. Investments qualify for ₹1.5 lakh deduction under Section 80C. 3-year lock-in.

Debt Mutual Funds Invest in government bonds, corporate bonds, treasury bills. Lower risk than equity. Returns of 6–8% typically. Better than FD for large investments (more tax efficient for investors in higher tax brackets).

Hybrid Funds Split between equity and debt. Aggressive Hybrid: 65–80% equity. Balanced Advantage Fund (BAF): dynamically adjusts

allocation based on market valuations. Good for first-time investors nervous about pure equity.

Index Funds Track a market index like Nifty 50 or Sensex passively. No fund manager picking stocks — just match the index. Very low expense ratio (0.1–0.2%). Warren Buffett's recommended strategy for most retail investors.Nifty 50 has delivered ~12% annualised returns over 20 years.

Sectoral / Thematic Funds Invest in specific sectors — technology, pharma, green energy, infrastructure. High conviction bets. Only for investors who understand the sector and have a 5+ year view.

What Is NAV in Mutual Funds?

NAV stands for Net Asset Value. It is the per-unit price

of a mutual fund on any given day.

Formula: NAV = (Total Assets of Fund − Liabilities) ÷

Total Number of Units Outstanding

Example: If a mutual fund holds ₹100 crore in stocks

and has issued 10 crore units, the NAV is ₹10 per unit.

Key things to understand about NAV:

A higher NAV does not mean a fund is expensive.

A fund with NAV ₹500 is not "costlier" than one

with NAV ₹10. What matters is the fund's performance

history and future potential, not its current NAV number.

NAV changes daily based on the closing price of the

fund's underlying stocks or bonds.

When you invest through SIP (Systematic Investment Plan),

you buy units at the NAV of the day your money is processed —

automatically, without trying to time the market.

A common beginner mistake: avoiding a mutual fund because

its NAV "seems too high." This is irrelevant. Focus on

the fund's 3-year and 5-year returns, expense ratio,

and fund manager track record instead.

Part 5 — Stocks: How to Make Money and What to Buy

How to Make Money in Stocks

There are two ways stocks generate returns:

Capital appreciation: You buy a share at ₹100. The company grows. The share rises to ₹300. You sell. You made ₹200 per share — a 200% return.

Dividends: Some companies distribute a portion of their profits to shareholders regularly. ITC, Coal India, and PSU banks are known for high dividend yields. This is passive income from stocks you continue to hold.

The honest truth about stock picking: Picking individual stocks consistently is extremely difficult. Studies consistently show that 80–90% of active fund managers underperform the Nifty 50 index over 10 years. Individual retail investors do even worse on average.

The correct framework for stock investing as a beginner:

Step 1: Build your core portfolio through Nifty 50 index funds or large-cap mutual funds via SIP. This is non-negotiable.

Step 2: Once you have 6+ months of SIP running and understand the basics, allocate a small "learning portfolio" — maybe 10–15% of your investment budget — to individual stocks you understand.

Step 3: Research before buying. Understand the company's business, revenue growth, profit margins, debt levels, and competitive position before buying a single share.

Step 4: Hold for 3–5 years minimum. Stocks are not a short-term instrument. Trading in and out generates transaction costs and taxes that destroy returns.

Stocks to Consider in 2026 — Themes Worth Watching

Rather than specific "stocks to buy today" (which change daily and require your own research), here are the structural themes with strong multi-year tailwinds in India:

Green Energy Stocks India has committed to 500 GW of renewable energy capacity by 2030. This is a multi-trillion rupee investment cycle. Companiesin solar manufacturing (Waaree Energies, Premier Energies), wind energy (Inox Wind, Suzlon), and green hydrogen are direct beneficiaries. Green energy is not a short-term trade — it is a decade-long structural theme.

Semiconductor Stocks India's semiconductor push — with Tata Electronics building a fab in Dholera and Micron's assembly plant in Sanand — is creating an entirely new industry vertical. Dixon Technologies, Kaynes Technology, and Tata Elxsi are positioned in India's electronics manufacturing ecosystem.

This theme could play out over 10–15 years.

Defence StocksAs covered in our market crash article, HAL, BEL, GRSE, and Mazagon Dock have long-term government order books regardless of market cycles. India's defence indigenisation programme is a 20-year tailwind.

Healthcare and Diagnostics Ageing population, rising health awareness, underpenetrated health insurance — Apollo Hospitals, Narayana Hrudayalaya,

Vijaya Diagnostics, and Medplus Health represent a structurally growing sector.

These are themes to research, not a buy list. Always do your own analysis or consult a SEBI-registered investment advisor before investing in individual stocks.

Part 6 — How to Invest in US Stocks from India

Yes, Indians can directly invest in Apple, Google, Amazon,

Nvidia, and Tesla from India. And in 2026, with the US being

the world's most innovative economy and the dollar being

the global reserve currency, having US stock exposure makes

genuine portfolio sense.

Two main routes:

Route 1: Direct US Stock Investment via International

Brokerage Apps

Platforms available to Indian investors:

— Vested Finance (Indian app, specifically built for

US stock investing from India)

— INDmoney (Indian app with US stock and ETF investing)

— Interactive Brokers (global platform, more complex

but full featured)

Under RBI's Liberalised Remittance Scheme (LRS), every

Indian resident can remit up to $250,000 per financial

year for investment purposes. This is more than enough

for any retail investor.

Tax note: A 20% TCS (Tax Collected at Source) is charged

on LRS remittances above ₹7 lakh per year. This is not

an additional tax — it is credited back against your

income tax liability when you file returns.

Capital gains from US stocks are taxed in India as

per your income tax slab (short term, held under 24 months)

or at 20% with indexation (long term, held over 24 months).

Route 2: US ETFs Available in India

Several Indian mutual funds now offer funds that invest

in US indices and stocks — without the LRS remittance process:

— Motilal Oswal Nasdaq 100 ETF / Fund of Fund

— Mirae Asset NYSE FANG+ ETF

— ICICI Prudential US Bluechip Equity Fund

— Kotak NASDAQ 100 Fund of Fund

These are denominated in INR, bought through your normal

Zerodha or Groww account, and taxed like debt mutual funds

(regardless of their equity nature, due to SEBI categorisation).

Best for most beginners: Start with an Indian Nasdaq 100

Fund of Fund via SIP. You get dollar diversification,

US tech exposure, and the simplicity of a domestic mutual fund.

Part 7 — Real Estate Investing in India

Real Estate Investing Tips

Real estate is India's most culturally beloved investment.

And for good reason — it has made genuine multi-generational

wealth for millions of Indian families.

But real estate in 2026 is a very different proposition than

it was in 2005. Here's what you actually need to know:

When real estate investing makes sense:

You have a 10+ year horizon. Real estate is deeply illiquid —

you cannot sell a flat in an emergency the way you can redeem

a mutual fund.

You have a 20–30% down payment ready in cash. Taking a

100% loan for an investment property at 9% interest rate

means your rental yield (typically 2–3% in Indian cities)

doesn't cover your interest cost. You're cash-flow negative

from day one.

You're buying in a high-growth micro-market with infrastructure

tailwinds — metro expansion, IT corridor development,

industrial zone creation. Location is everything in real estate.

Real estate investing tips for Indian buyers:

Check RERA registration before booking any under-construction

property. Rera.gov.in — verify the project is registered

and the builder hasn't violated timelines.

Calculate the actual yield: Annual rent ÷ Property price

= Gross yield. In Mumbai, a ₹1 crore flat renting for

₹25,000/month gives a 3% gross yield — before maintenance,

vacancy, and taxes. Compare this honestly to a mutual fund.

Factor in total cost of ownership: Stamp duty (5–7% of

property value), registration, interiors, maintenance,

society charges, property tax — these are not small numbers.

Consider tier-2 cities: Pune, Hyderabad, Ahmedabad, Indore,

Coimbatore — better yield-to-price ratios than Mumbai or

Delhi, with growing IT and manufacturing employment bases.

How to Invest in Real Estate Without Buying Property

If you want real estate exposure without the ₹50 lakh –

₹1 crore commitment, there are two modern alternatives:

REITs (Real Estate Investment Trusts)

REITs are listed on Indian stock exchanges and let you

invest in commercial real estate — office parks, malls,

data centres — starting with as little as ₹300–₹400

per unit.

India's listed REITs as of 2026:

Embassy Office Parks REIT — India's largest, with

Grade-A office space leased to MNCs.

Mindspace Business Parks REIT — Offices in Hyderabad,

Pune, Mumbai.

Brookfield India REIT — Large commercial campuses

in Delhi NCR, Mumbai, Kolkata.

Nexus Select Trust REIT — India's first retail

(mall) REIT.

REITs must distribute at least 90% of their income

to investors as dividends — making them an income

instrument, not just a capital appreciation play.

Current yield: 6–8% per year plus potential appreciation.

Real Estate Business via Fractional Ownership Platforms

Platforms like hBits, Strata, and PropertyShare allow

investors to own a fraction of a commercial property —

a ₹10 crore office building shared across 100 investors

at ₹10 lakh each. Returns include rent yield (8–10%)

plus capital appreciation.

Minimum investment: ₹10–₹25 lakh. Not for beginners,

but worth knowing for when you're further along.

Part 8 — I'm 25 and Earning ₹30,000 a Month. Exactly How Should I Start?

This is the most important section of this article.

If you're 25 and earning ₹30,000 a month, here is the exact framework — not generic advice, but specific allocations:

First: Build your foundation (Month 1–3)

Emergency Fund: Save 3 months of expenses (roughly ₹40,000–₹50,000 for most people in this income bracket) in a high-interest savings account or liquid mutual fund.AU Small Finance Bank savings account (7%+) or Mirae Asset Cash Management Fund.

Aadhaar-linked bank account ✅

PAN card ✅

KYC completed on Zerodha or Groww (or any other broker platform)✅

This takes 2–3 months to build. Don't invest in equity until this is done. It is your financial airbag.

Then: Your monthly allocation on ₹30,000 income

Rent + utilities + food: ₹15,000–₹18,000

Emergency fund top-up (if not complete): ₹5,000

SIP — Nifty 50 Index Fund: ₹3,000

SIP — ELSS (tax saving + long-term growth): ₹2,000

Gold ETF or SGB SIP: ₹1,000

Liquid buffer (unexpected expenses): ₹1,000–₹2,000

Total investable: ₹6,000–₹7,000/month.

This is not dramatic. But ₹6,000/month in a Nifty 50 index fund starting at age 25, at 12% annual return, becomes ₹3.5 crore by age 55.

The number isn't the point. The habit is the point.

What to avoid at 25:

— Crypto as a primary investment (speculation, not investing)

— F&O trading (92% of retail F&O traders lose money,

per SEBI's own data)

— Chit funds and MLM "investment" schemes

— Keeping more than 3 months expenses in a savings account

As your income grows — and at 25, it will — increase your SIP amount by at least 10% every year. This single habit, called "SIP step-up," is the most powerful wealth-building decision available to a salaried Indian.

The Tool That Connects Saving and Investing — Tracking

Here's the uncomfortable truth about personal finance in India:

most people who read articles like this one take no action

afterward.

Not because they don't want to. But because they don't know

their actual numbers.

They don't know how much they're currently spending vs saving.

They don't know if their emergency fund is actually 3 months

of expenses or 1.5 months.

They don't know how much of their salary is disappearing

into UPI transfers, subscriptions, and food orders before

they get a chance to invest it.

Without that clarity, every financial decision is guesswork.

RozHisab is built specifically for this — to give you that

clarity.

Track every income and expense in one place.

See exactly how much you're saving each month versus how

much you should be saving.

Set investment targets (your ₹6,000/month SIP goal) and

track whether you're hitting them.

See your complete financial picture — savings account

balance, SIP progress, emergency fund status — in one view.

The best financial plan in the world doesn't work if you

don't know whether you're executing it.

Start tracking at RozHisab — free, no ads, built for Indian users.

The One-Page Summary — Savings vs Investing

When to save (use savings account / FD / RBI bonds):

— Emergency fund (3–6 months expenses): Savings account

or liquid mutual fund

— Money needed in next 1–2 years: FD or RBI bonds

— Conservative investors who cannot tolerate any loss:

RBI Floating Rate Bonds at 8.05%

When to invest (mutual funds / stocks / real estate / US stocks):

— Money you won't need for 5+ years: Equity mutual funds

— Tax saving: ELSS mutual funds (80C benefit)

— Inflation hedge: Gold ETF or SGB

— Dollar diversification: US index funds via INDmoney/Vested

— Income + real estate exposure without locking ₹1 crore: REITs

— Long-term wealth creation: Nifty 50 index fund SIP

The core principle:

Save for security. Invest for freedom.Both are necessary. The ratio shifts as your income grows — but the habit starts with your very first paycheck,

no matter how small.