₹25,000 a month. That is ₹833 per day to cover rent, food, transport, phone, clothes, family obligations, emergencies, and — if anything is left — savings and investments.

Most people at this salary level believe saving is impossible. They are wrong.

Thousands of Indians earning ₹25,000/month are building emergency funds, running SIPs, and living without financial stress — not because they earn more, but because they know exactly where every rupee goes.

The difference between financial stress and financial stability at ₹25,000/month is not income. It is a working budget that you actually follow.

This article gives you that budget — with exact numbers, real expense breakdowns, tax saving strategies for salaried employees, and a system to track it all without spending hours on spreadsheets.

First — Understand Your Actual In-Hand Salary

Salary Slip — What It Means and Why It Matters for Budgeting

Before budgeting a single rupee, you need to know your actual take-home amount — not your CTC (Cost to Company), not your gross salary, but the number that hits your bank account every month.

Your salary slip is the document that shows this breakdown. Every salaried employee in India receives a salary slip every month — either physically or via email/HR portal. If you've never looked at yours carefully, now is the time.

Key components of a salary slip in India:

- Basic Salary: The fixed core component — typically 40–50% of CTC. This is what PF, gratuity, and HRA are calculated on.

- HRA (House Rent Allowance): Paid to cover rent costs. If you live in rented accommodation and pay rent, this component is partially or fully tax-exempt.

- Special Allowance / Other Allowances: Flexible components that make up the balance of your gross salary. Usually fully taxable.

- PF Deduction (Provident Fund): 12% of Basic Salary deducted and matched by employer. Goes into your EPF account — this is forced savings you don't see in hand but is working for you.

- TDS (Tax Deducted at Source): Income tax deducted by employer based on your estimated annual tax liability. At ₹25,000/month (₹3 lakh annual CTC), TDS is typically zero or minimal due to tax rebates.

- Net Salary / In-Hand: What actually reaches your bank account after all deductions.

⚠️ Important: If your CTC is ₹25,000/month but your in-hand is ₹21,000–₹22,000 after PF and other deductions — budget on the in-hand number, not the CTC. This is the mistake that breaks most people's budgets before they even start.

For this article, we assume ₹25,000 as your actual in-hand monthly salary — the amount credited to your bank account.

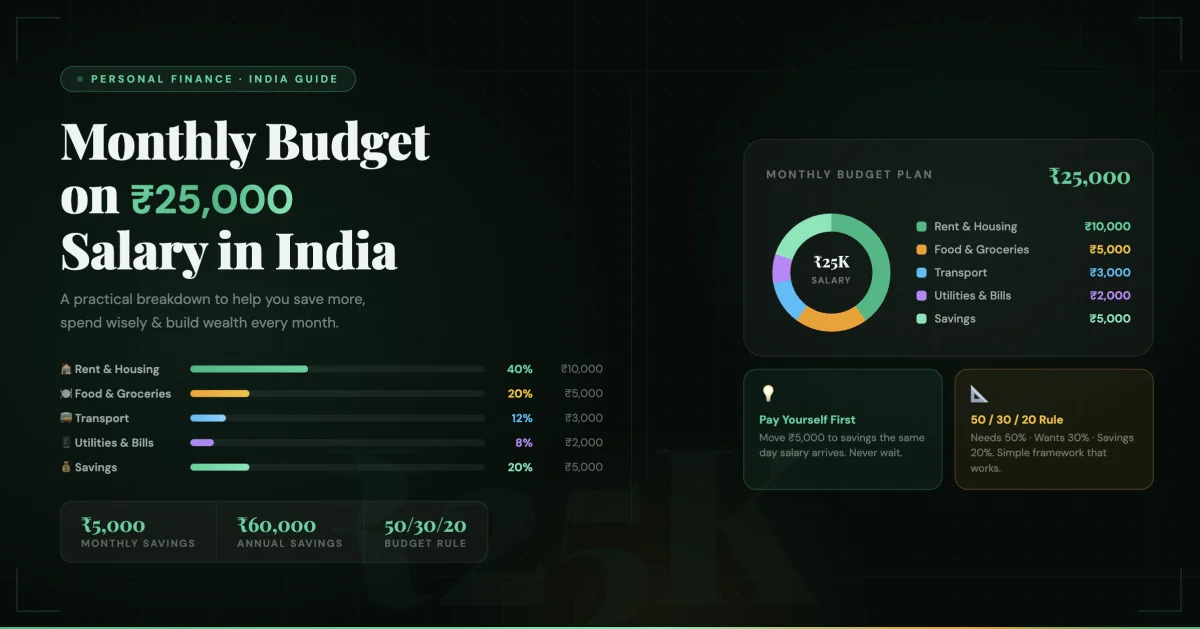

The ₹25,000 Monthly Budget — Exact Breakdown

Here is a realistic, city-appropriate budget for a single person earning ₹25,000/month in an Indian metro or tier-2 city. Adjust the numbers to your specific city and living situation.

The 50-30-20 Framework Adapted for India

The classic 50-30-20 rule says: 50% on needs, 30% on wants, 20% on savings. In India at ₹25,000, the rent-to-income ratio in most cities makes a strict 50-30-20 difficult. Here is a more realistic 60-20-20 framework for ₹25,000:

- 60% (₹15,000) — Essential Needs

- 20% (₹5,000) — Lifestyle and Wants

- 20% (₹5,000) — Savings and Investments

Here is what that looks like with actual rupee amounts:

Category 1 — Essential Household Expenses (₹15,000)

Household expenses are the non-negotiable costs of running your life every month. These must be covered first before any other spending decision is made.

Rent: ₹6,000–₹8,000

This is the single largest household expense for most

Indians at this income level. In metro cities (Mumbai,

Delhi, Bangalore), a PG or shared accommodation in

a decent area runs ₹6,000–₹10,000. In tier-2 cities

(Pune outskirts, Jaipur, Indore, Coimbatore),

a 1BHK is available at ₹6,000–₹8,000.

Target: Keep rent below 35% of in-hand salary.

At ₹25,000, that means rent below ₹8,750.

Groceries and Cooking at Home: ₹2,500–₹3,000

Cooking your own meals is the single most effective

cost-reduction strategy available at this income level.

A person cooking at home in India can eat well on

₹80–₹100/day — ₹2,500–₹3,000/month including

vegetables, dal, rice, oil, and occasional non-veg.

Transport: ₹1,500–₹2,500

Monthly pass for metro/bus: ₹500–₹900 depending on city.

Two-wheeler petrol (if you own one): ₹600–₹1,000/month

for daily commuting.

Ola/Uber supplement: ₹500–₹800/month.

If you own a two-wheeler, keep it well-maintained —

a poorly maintained bike uses 20–30% more fuel.

Electricity, Water, Internet, Mobile: ₹1,200–₹1,800

Electricity (shared/PG): ₹300–₹600

Mobile recharge (data + calls): ₹200–₹350

Broadband internet (if not included in rent): ₹400–₹600

Water/maintenance (if applicable): ₹100–₹200

Household Expenses Meaning — What Counts:

Household expenses include all recurring costs

required to maintain your daily living — rent,

utilities, groceries, transport, and basic personal care.

They do NOT include dining out, entertainment,

clothing, or subscriptions — those fall under lifestyle spending.

Total Essential Expenses: ₹11,200–₹15,300

Target: Stay below ₹15,000 (60% of ₹25,000).

Category 2 — Lifestyle and Wants (₹5,000)

This is the category most people overspend in — and the first place to cut when savings targets are missed.

Dining out and food delivery: ₹1,000–₹1,500

At ₹25,000/month, limiting Swiggy/Zomato orders to

4–6 times per month (₹150–₹250 per order) is a

realistic and sustainable target. Daily ordering

at this salary level is a budget killer —

₹150/day on food delivery = ₹4,500/month

on food alone, before any cooking at home.

Clothing and personal care: ₹800–₹1,200

Monthly average across the year. Some months zero,

some months ₹2,000–₹3,000. Budget on

a monthly average, not transaction by transaction.

Entertainment and subscriptions: ₹500–₹800

Netflix/Disney+/YouTube Premium, movies, weekend

outings. Share subscriptions with roommates

or family to cut this in half.

Miscellaneous expenses: ₹500–₹1,000

Miscellaneous expenses are small,

irregular costs that don't fit neatly into other

categories — a haircut, a medical co-pay,

a birthday gift, a book. Every budget needs a

miscellaneous buffer. Without it, these small

costs blow your budget every month and you never

understand why.

Total Lifestyle Spending: ₹2,800–₹4,500

Target: Stay below ₹5,000 (20% of ₹25,000).

Category 3 — Savings and Investments (₹5,000)

This is the category that builds your future. It must be treated as an expense, not a leftover. The biggest budgeting mistake Indians make is saving what's left after spending — instead of spending what's left after saving.

Emergency Fund (Priority 1): ₹2,000–₹3,000/month

Before any investment, build an emergency fund of

3 months of expenses — approximately

₹35,000–₹45,000 for someone on ₹25,000/month.

Keep this in a high-interest savings account

(AU Small Finance Bank, Equitas — offering 6.5–7%+)

or a liquid mutual fund.

At ₹2,000–₹3,000/month, this takes 12–18 months

to build fully. Once built, redirect this amount to investments.

SIP in Nifty 50 Index Fund (Priority 2): ₹1,000–₹2,000/month

Once emergency fund is established, start a SIP

in a Nifty 50 index fund — Nippon India Index Fund,

UTI Nifty 50, or HDFC Index Fund.

₹1,000/month at 12% annual returns

for 20 years = approximately ₹9.9 lakh.

This is not glamorous. It is wealth-building.

ELSS Tax Saving SIP (Priority 3): ₹500–₹1,000/month

If you're in the old tax regime and have taxable

income after standard deduction, ELSS gives you

a Section 80C deduction while building equity wealth.

At ₹25,000/month gross, your taxable income may

already be below the basic exemption limit —

but if not, ELSS is your first investment after

the emergency fund.

Total Savings and Investments: ₹3,500–₹6,000

Target: Minimum ₹5,000 (20% of ₹25,000).

How to Save Tax on Salary at ₹25,000/Month

Tax Saving for Salaried — The Good News at This Income Level

Here is the best financial news for someone earning ₹25,000/month (₹3 lakh annual salary):

You likely owe zero income tax.

Under both old and new tax regimes, income up to ₹2.5 lakh is tax-free. After the standard deduction of ₹50,000 for salaried employees, your taxable income at ₹3 lakh annual CTC is just ₹2.5 lakh — right at the basic exemption limit.

Additionally, Section 87A provides a full tax rebate for income up to ₹7 lakh under the new regime — meaning even if your taxable income is slightly above ₹2.5 lakh, you still pay zero tax.

Tax saving salary structure tips for ₹25,000/month:

- Claim HRA exemption if you live in rented accommodation — submit rent receipts to your employer every year. Even at this salary, HRA can reduce your taxable income.

- Submit investment proof on time — your employer deducts TDS based on declared investments. If you don't submit proof, they deduct TDS on full salary. Submit EPF, LIC, and ELSS receipts to HR before the deadline (usually January–February).

- Check Form 16 carefully — your employer issues Form 16 after year-end showing all deductions. Verify every component before filing ITR.

Monthly Budget Calculator — The Simple Version

Here is your monthly budget calculator framework for ₹25,000 in-hand salary:

- 💰 In-hand salary: ₹25,000

- 🏠 Rent: ₹7,000 (28%)

- 🛒 Groceries: ₹2,500 (10%)

- 🚌 Transport: ₹2,000 (8%)

- ⚡ Utilities + Mobile + Internet: ₹1,500 (6%)

- 🍔 Dining out + Food delivery: ₹1,500 (6%)

- 👕 Clothing + Personal care: ₹1,000 (4%)

- 🎬 Entertainment + Subscriptions: ₹500 (2%)

- 📦 Miscellaneous expenses: ₹500 (2%)

- 🏦 Emergency fund SIP: ₹2,500 (10%)

- 📈 Investment SIP: ₹2,000 (8%)

- ⚠️ Buffer / Unexpected: ₹1,500 (6%)

- Total: ₹26,000 ← Adjust rent or lifestyle to fit your exact income

This is a house monthly budget — a template, not a rigid rule. Your rent may be higher or lower. Your transport costs depend on your commute. The percentages matter more than the absolute numbers. Keep essential expenses below 60%, lifestyle below 20%, and protect the 20% savings no matter what.

Direct Expenses vs Prepaid Expenses — Know the Difference When Budgeting

Direct expenses are costs that happen in the current month and are paid immediately — groceries, electricity bill, petrol, dining out. These are easy to track because the payment and consumption happen together.

Prepaid expenses are costs you pay upfront but consume over time — annual insurance premium, annual subscriptions (Amazon Prime, gym membership), advance rent. In personal budgeting, always convert prepaid expenses to a monthly equivalent when building your budget. If you pay ₹12,000 for annual insurance once a year, that is ₹1,000/month in your budget — even though you don't pay it every month. Without this conversion, your budget will look fine 11 months a year and then blow up catastrophically in the one month the annual payment hits.

The 4 Habits That Make or Break a ₹25,000 Budget

Habit 1 — Pay yourself first

On the day your salary is credited, immediately

transfer your savings amount — ₹5,000 in this

framework — to a separate savings account or

liquid fund. What's in your spending account

is what you have to spend. You cannot overspend

money that's already moved.

Habit 2 — Use cash or UPI limits for lifestyle categories

Set a monthly UPI spending limit notification

on your phone (most banking apps allow this).

When you're approaching your ₹5,000 lifestyle

limit, you'll get a notification — before you

overspend, not after.

Habit 3 — Review every Sunday for 10 minutes

Once a week, check what you've spent so far

in the month versus your budget. 10 minutes

every Sunday prevents the month-end shock

of running out of money with 10 days left.

Catching overspending on day 10 gives you

20 days to correct. Catching it on day 25 is too late.

Habit 4 — Track every expense,

especially the small ones

A ₹50 chai here. A ₹120 auto ride there.

A ₹200 impulse purchase at a store.

Individually these feel insignificant.

Cumulatively, small untracked expenses

account for ₹2,000–₹4,000 of mystery spending

every month for most people. When you track them,

you see the pattern — and the pattern is fixable.

Household Expenses App — The Missing Piece in Most People's Budget

The reason most budgets fail is not lack of knowledge or lack of intention. It is lack of a system to track spending in real time.

A budget written in a notebook on the 1st of the month and checked on the 30th is not a budget — it is a post-mortem. By then the money is already gone.

What actually works is logging expenses as they happen — at the billing counter, in the auto, at the grocery store — so your running total is always visible.

Use RozHisab as your household expenses app. Log every transaction — rent, groceries, transport, dining, miscellaneous — and see your real-time spending against your monthly budget in one place. When you've spent ₹3,800 of your ₹5,000 lifestyle budget on the 18th of the month, you know to slow down — before you overshoot, not after.

RozHisab is built specifically for Indian households — with Indian expense categories, Indian salary structures, and a completely free model with no ads. It takes 2 minutes to set up and 30 seconds per day to maintain.

What to Do When the Budget Doesn't Balance

In some cities and living situations, the numbers above simply don't work. Rent alone in Mumbai or Bangalore can be ₹10,000–₹12,000 for basic accommodation — leaving almost nothing for everything else.

If your essential expenses consistently exceed 60% of your income, here are the levers to pull — in order of impact:

Lever 1 — Reduce rent (highest impact)

Rent is the single largest variable in this budget.

Moving to a shared accommodation, a PG,

or a slightly longer commute that allows a cheaper

locality can free up ₹2,000–₹4,000/month immediately.

This is the one change with the highest ROI

on a ₹25,000 budget.

Lever 2 — Eliminate food delivery

Daily Swiggy/Zomato is a ₹3,000–₹5,000/month habit

at typical order sizes. Cooking at home for weekday

meals and allowing one weekend delivery order is

a realistic middle ground that saves ₹1,500–₹2,500/month.

Lever 3 — Cut subscriptions you don't actively use

Audit every monthly subscription. Netflix,

Hotstar, Spotify, Amazon Prime, gym membership —

list them all and cancel anything you haven't

actively used in the last 2 weeks.

Most people have ₹500–₹1,200/month

in subscriptions they've forgotten about.

Lever 4 — Increase income, not just cut expenses

At ₹25,000/month, a 10% salary hike or a small

freelance income of ₹2,000–₹3,000/month changes

the math significantly. Upskilling, certifications,

or freelance work on weekends is worth considering

if the budget consistently doesn't balance after

all cuts are made.

The One Number That Matters More Than Your Budget

After all the categories, rules, and percentages — there is one number that tells you whether your budget is actually working:

Your monthly savings rate.

Savings rate = (Amount saved ÷ In-hand salary) × 100

At ₹25,000/month:

- Saving ₹2,500/month = 10% savings rate — minimum acceptable

- Saving ₹5,000/month = 20% savings rate — good, on track

- Saving ₹7,500/month = 30% savings rate — excellent, wealth-building pace

Track this number every single month. If your savings rate is increasing over time — even slowly — your financial life is improving. If it's decreasing or zero, something in the budget needs to change before lifestyle inflation permanently anchors your expenses at income level.

Use RozHisab to see your savings rate automatically every month — log your income and expenses and it calculates what percentage you're saving without any manual calculation. When you can see your savings rate clearly every month, it becomes a number you want to improve — and that motivation is what makes budgets stick long term.

👉 Start your free budget tracker at RozHisab — track every household expense, see your savings rate in real time, and finally know exactly where your ₹25,000 goes every month.

Quick Reference — ₹25,000 Monthly Budget Cheatsheet

- 🏠 Rent: Max ₹8,750 (35% of income)

- 🛒 Groceries: ₹2,500 — cook at home daily

- 🚌 Transport: ₹2,000 — monthly pass + petrol

- ⚡ Utilities: ₹1,500 — internet + mobile + electricity

- 🍔 Food delivery: Max ₹1,500 — max 6 orders/month

- 📦 Miscellaneous expenses: ₹500 buffer — always include this

- 🏦 Emergency fund first: ₹2,000–₹3,000 until ₹40,000 is saved

- 📈 SIP investment: ₹1,000–₹2,000 — Nifty 50 index fund

- 💡 Savings rate target: Minimum 20% (₹5,000/month)

- 📱 Track everything: Use RozHisab — free household expenses app

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →