ℹ️ Note: This article is for general educational and informational purposes only. All app comparisons, budget figures, and expense examples are illustrative. Financial habits and results vary by individual. Nothing in this article constitutes financial advice. RozHisab is a personal finance tracking tool — not an investment advisory service.

Here is a question most Indians can't honestly answer:

"Where exactly did your salary go last month?"

Not roughly. Not "rent, food, and some shopping." Exactly — with rupee amounts, by category, broken down by week.

If you can't answer that question, you are not alone. Studies consistently show that most salaried Indians have no accurate picture of their monthly spending — even those earning well above average.

The result: month-end stress, mysterious account balance drops, the vague feeling that you should be saving more but somehow never do, and the annual shock of realising you have nothing meaningful saved despite a decent income.

The solution is not earning more. It is knowing where every rupee goes — and the system to do that is simpler than most people think.

This article covers every method of tracking daily expenses in India — from the traditional hisab kitab notebook to Google Sheets to dedicated apps — and helps you find the one system that will actually stick for your lifestyle.

Why Most Indians Stop Tracking Expenses After 3 Days

Before getting into the how, understand the why of failure. Most people who try to track expenses quit within a week. The reasons are consistent:

1. The system requires too many steps

Opening an app, selecting a category,

entering an amount, adding a note,

saving — five steps for every

₹20 auto ride. By day three,

it feels like a second job.

2. They start with too much complexity

Creating 25 expense categories on day one.

Splitting grocery bills between

"vegetables," "dairy," "grains,"

and "packaged food." This level of

granularity is useful for accountants,

not for someone trying to build

a basic financial habit.

3. They miss one day and give up

Skipped logging Saturday's expenses.

Now the record is incomplete.

Feels pointless to continue.

This is a mindset problem,

not a system problem.

An 80% complete expense record

is infinitely more useful

than zero record at all.

4. The system doesn't match

Indian spending patterns

Most international budgeting apps

have categories designed for

Western spending — mortgage,

401k, health insurance.

Indian household spending includes

EMIs, UPI transfers to family,

festival expenses, domestic help,

and cash transactions at local

kiranas that don't generate

digital records automatically.

The right expense tracking system for an Indian household needs to be: fast (under 30 seconds per entry), flexible (handles cash + UPI + cards), and forgiving (works even if you miss a day or two).

What Is Hisab Kitab — And Why Every Indian Already Understands Expense Tracking

Hisab Kitab in English

Hisab Kitab is a Hindi/Urdu phrase meaning "accounts book" or "ledger of accounts." Hisab = accounts, calculation, reckoning. Kitab = book.

Literally translated to English: hisab kitab means "the book of daily accounts" — a record of all money coming in and going out, maintained daily.

Before smartphones, before Excel, before any app — Indian households maintained hisab kitab. A simple notebook. Two columns. Income on one side, expenses on the other. Every shopkeeper, every household, every small business ran on this system for generations.

The concept is not new. The tools have changed. But the underlying habit — writing down every rupee that moves through your hands — is exactly what every modern expense tracking system is trying to replicate digitally.

RozHisab is named from this exact tradition. Roz (daily) + Hisab (accounts) = daily accounting. The name is the philosophy: track every day, in the same way your parents and grandparents tracked every day — just without the notebook.

Hisab Kitab Book — The Traditional Method

If you prefer pen and paper — a physical hisab kitab book is a completely valid system. Here is how to set it up in 5 minutes:

Page setup — draw 4 columns:

- Date (narrow column)

- Description (what you spent on — 2-3 words only)

- Amount (in ₹)

- Category (Food / Transport / Bills / Shopping / Other)

Daily routine — takes 3 minutes:

Every night before sleeping,

open the book and write down

every expense from the day.

Use UPI transaction history on

your phone as a reference for

digital payments. For cash,

keep a running mental note

or use the Notes app during the day.

Weekly review — takes 10 minutes:

Every Sunday, add up the week's

expenses by category. Note which

category surprised you most.

That category is where your

budget needs the most attention.

The physical hisab kitab works surprisingly well for people who spend primarily in cash or at local markets. Its limitations: no automatic calculations, no charts, no reminders, and no backup if the book is lost.

Daily Expense Tracker Excel — The Spreadsheet Method

Daily Expense Tracker Excel — Basic Setup

For people comfortable with computers, a daily expense tracker in Excel or Google Sheets gives more analytical power than a notebook with almost as much simplicity.

Simple daily expense sheet structure — 6 columns:

- Column A: Date

- Column B: Description (e.g., "Swiggy dinner," "Auto to office")

- Column C: Category (dropdown list — use Data Validation in Excel/Sheets to set this up)

- Column D: Amount (₹)

- Column E: Payment Mode (Cash / UPI / Card)

- Column F: Notes (optional — for unusual expenses)

Daily expense format —

how to enter data:

One row per transaction.

Don't try to combine.

"Groceries and coffee" as one

₹450 entry is useless data.

"Big Bazaar groceries ₹380"

and "Coffee ₹70" as two rows

is useful data.

Monthly summary tab —

the most useful part:

Create a second tab with

SUMIF formulas that automatically

total each category across the month.

In Google Sheets, this formula

totals all "Food" category expenses:

=SUMIF(Sheet1!C:C,"Food",Sheet1!D:D)

Do this for each category and you have a live monthly expense summary that updates every time you add a row on the main tab.

Expense Tracker Google Sheets — Advantages Over Excel

Google Sheets has one critical advantage over Excel for expense tracking: it works on every device simultaneously.

You can open the same Google Sheet on your phone in the auto, add an expense row in 20 seconds, and see it immediately updated on your laptop when you check the monthly summary at night.

Google Sheets expense tracker setup:

- Go to sheets.google.com → create a new blank sheet

- Set up the 6-column structure above

- Add a dropdown for Category column: select the category column → Data → Data Validation → List of items → type your categories separated by commas

- Bookmark the sheet on your phone's home screen as a web app — tap to open instantly, no app download required

- Share the sheet with your spouse or family member so both can add expenses to the same tracker simultaneously

Free Google Sheets templates

for Indian households:

Search "monthly budget India Google Sheets"

on Google — several free templates

exist with pre-built Indian expense

categories (EMI, domestic help,

festival budget, etc.)

that you can copy and customise.

Limitation of Excel and Google Sheets: Both require manual entry on a laptop or phone browser. There is no push notification reminder to log expenses. No automatic UPI import. No visual dashboard. For people who want automation and a better mobile experience, a dedicated app is the next step.

Daily Expense Manager Apps — What to Look for and What to Avoid

What Is a Daily Kharcha App?

Kharcha is the Hindi word for "expense" or "expenditure." A daily kharcha app is simply a daily expense tracking application — the digital version of the hisab kitab notebook.

The ideal daily expense manager for an Indian user has these features:

- ✅ Quick entry in under 10 seconds — amount, category, done. No mandatory description, no multiple screens.

- ✅ Indian expense categories — EMI, domestic help, vehicle fuel, festival expenses, family transfer — not just Western categories like "subscription" and "gym."

- ✅ UPI and SMS parsing — reads your bank SMS alerts to auto-import transactions without manual entry.

- ✅ Cash expense support — Indian households still use significant cash. The app must handle cash entries alongside digital payment tracking.

- ✅ Multiple account support — salary account, savings account, spouse's account, credit card — all in one view.

- ✅ Monthly summary with visual charts — shows where money went by category, so the insight is immediate, not buried in rows of data.

- ✅ Free — no paywall for basic tracking — most Indian households don't need advanced features. Core tracking should be free.

Hisab Kitab App — The Digital Version of the Traditional System

Several apps in India use "Hisab Kitab" or similar naming — recognising that Indian users respond to this framing more than Western terms like "personal finance manager."

The best hisab kitab app for an Indian household is one that replicates the simplicity of the paper notebook — but with automatic totals, category breakdowns, and the ability to track from your phone in 10 seconds flat.

What to avoid in expense tracking apps:

- 🚫 Apps that require account linking via bank credentials — sharing your net banking login with a third-party app is a significant security risk

- 🚫 Apps with aggressive premium paywalls that hide basic monthly summaries behind subscriptions

- 🚫 Apps designed for US/UK markets with no Indian currency, Indian bank, or Indian payment mode support

- 🚫 Apps that bombard you with financial product advertisements disguised as "insights"

Income and Expense Tracker — The Complete Picture Beyond Just Expenses

Tracking expenses alone gives you half the picture. The full picture requires tracking both income and expenses together — because the number that matters most is not how much you spent, but how much you saved.

Income sources to track for an Indian salaried household:

- Monthly salary (in-hand, after deductions)

- Freelance or side income

- Rental income (if any)

- Interest income (savings account, FD)

- Dividend income (from stocks or mutual funds)

- Family transfers received

The monthly savings rate formula:

Savings Rate =

((Total Income − Total Expenses) ÷ Total Income) × 100

Example:

In-hand salary: ₹45,000

Total expenses logged: ₹34,000

Savings: ₹11,000

Savings rate: (₹11,000 ÷ ₹45,000) × 100

= 24.4%

When you track both income and expenses, this number appears automatically every month. It tells you — clearly and without ambiguity — whether your financial life is improving or deteriorating. A rising savings rate over time is the single most important indicator of financial health for a salaried Indian household.

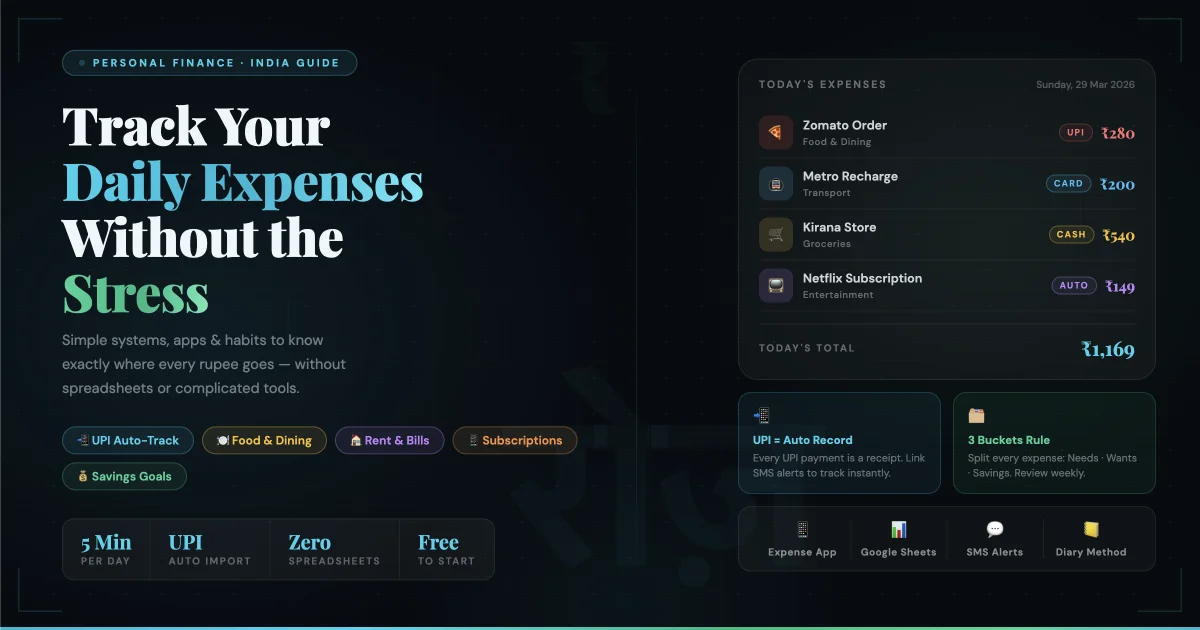

Daily Expenses Format — The 5-Category System That Actually Works

Most expense tracking systems fail because they have too many categories. Twenty-five categories sounds thorough. In practice, it means every expense requires a decision — "Is this food or entertainment? Is this a household expense or a personal expense?" Decision fatigue kills the habit.

Here is the 5-category system that is specific enough to be useful and simple enough to be sustainable:

Category 1 — Essentials (Non-negotiable)

Rent, EMI, electricity, gas,

water, internet, mobile recharge,

groceries, domestic help salary.

Things that happen every month

regardless of any other decision.

Category 2 — Food & Dining

Everything food-related that

is not grocery shopping —

restaurants, Swiggy/Zomato,

chai tapri, office canteen,

snacks outside home.

This is the category that

surprises most people

when they see the monthly total.

Category 3 — Transport

Petrol, auto/cab fares,

metro/bus pass, vehicle maintenance,

parking charges. Tracked separately

because it's often the second

or third highest category

for urban Indians.

Category 4 — Lifestyle

Shopping (clothes, electronics,

home items), entertainment

(movies, events, OTT subscriptions),

personal care (salon, gym),

gifts, and miscellaneous.

Everything that is a choice

rather than a necessity.

Category 5 — Savings & Investments

SIP deductions, FD deposits,

RD contributions, insurance premiums.

Treat this as an expense category —

because it must be protected

from the other four categories

overspending.

The daily expenses diary approach:

At the end of every day,

open your app or notebook,

recall every expense,

assign it to one of these five categories,

enter the amount.

Total time: 2–4 minutes per day.

Total insight gained: complete

visibility into your financial life.

Money Manager Expense and Budget — Choosing the Right System for Your Life

Match your system to your behaviour, not to what looks most impressive:

If you are a pen-and-paper person:

→ Physical hisab kitab notebook.

Buy a small diary.

Keep it beside your bed.

Fill it every night.

Simple, zero technology,

works without internet.

If you are comfortable with spreadsheets:

→ Google Sheets expense tracker.

One shared sheet for the household.

Bookmark it on your phone.

Update throughout the day

or batch-enter every evening.

If you want automation and a mobile-first experience:

→ Dedicated Indian expense tracking app.

Look for SMS parsing, Indian categories,

UPI support, and a clean

monthly summary dashboard.

RozHisab is built specifically

for this — a daily hisab kitab

for the Indian household,

free and without ads.

If you are completely new to tracking:

→ Start with the simplest possible system.

One Notes app note per day.

List every expense with amount.

Total it at month end.

After 2 months of this habit,

graduate to a proper system.

Starting imperfectly is infinitely

better than not starting at all.

The One Habit That Makes Every System Work

The tracking system you choose matters less than the habit you build around it. The most powerful tracking habit in personal finance is the 3-minute daily review:

Every night — before sleeping, while charging your phone, during the last ad break — open your expense tracker and log everything from the day. Not the week. Not the month. The day.

When you review daily:

- No expense is forgotten (memory of spending fades fast — a 2-day-old auto fare is gone from memory; a 2-hour-old one is clear)

- You catch overspending in real time — on day 15, not day 31

- The habit becomes automatic within 21 days — it stops feeling like effort and starts feeling like brushing teeth

- Month-end totals stop being surprises and start being expected numbers you already roughly know

The people who successfully track expenses for years are not financial enthusiasts. They are people who found a system simple enough to maintain daily — and maintained it long enough for it to become effortless.

RozHisab — Daily Hisab Kitab Built for Indian Households

Every system described in this article works. The question is which one you will actually maintain for more than 2 weeks.

RozHisab is built around the same principle as the traditional hisab kitab — simple daily accounting, designed for how Indian households actually spend money.

Track income and expenses in one place. See your monthly summary by category. Know your savings rate automatically. Manage multiple accounts — salary, savings, cash — in one free dashboard.

No bank credential sharing. No aggressive upselling. No ads. Free forever.

Because roz ka hisab — daily accounts — is not a complicated financial concept. It is the simplest, most proven habit in personal finance. And it has been working for Indian households for generations — long before any app existed.

👉 Start your daily hisab kitab at RozHisab — free, built for India, no jargon, no complexity. Just your daily expenses tracked clearly, every single day.

Quick Reference — Daily Expense Tracking Options for India

- 📓 Physical hisab kitab notebook: Best for cash spenders, pen-and-paper preference, zero technology comfort

- 📊 Daily expense tracker Excel: Best for desktop users, analytical mindset, want custom calculations

- 🌐 Expense tracker Google Sheets: Best for families who want shared tracking, mobile + desktop, free with auto-formulas

- 📱 Daily kharcha app: Best for mobile-first users, want SMS auto-import, need visual monthly summaries

- 🇮🇳 RozHisab: Best for Indian households wanting a hisab kitab app that is free, ad-free, and built for Indian spending patterns

- ⏱️ Time required daily: 2–4 minutes. That is the only investment required to know exactly where every rupee goes.

- 🎯 The only rule that matters: Log every day. Miss a day — continue the next day. An imperfect record is worth infinitely more than no record.

📌 Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. All budget figures and examples are illustrative. Individual financial situations vary. RozHisab is a budgeting and expense tracking tool — not an investment advisory service.

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →