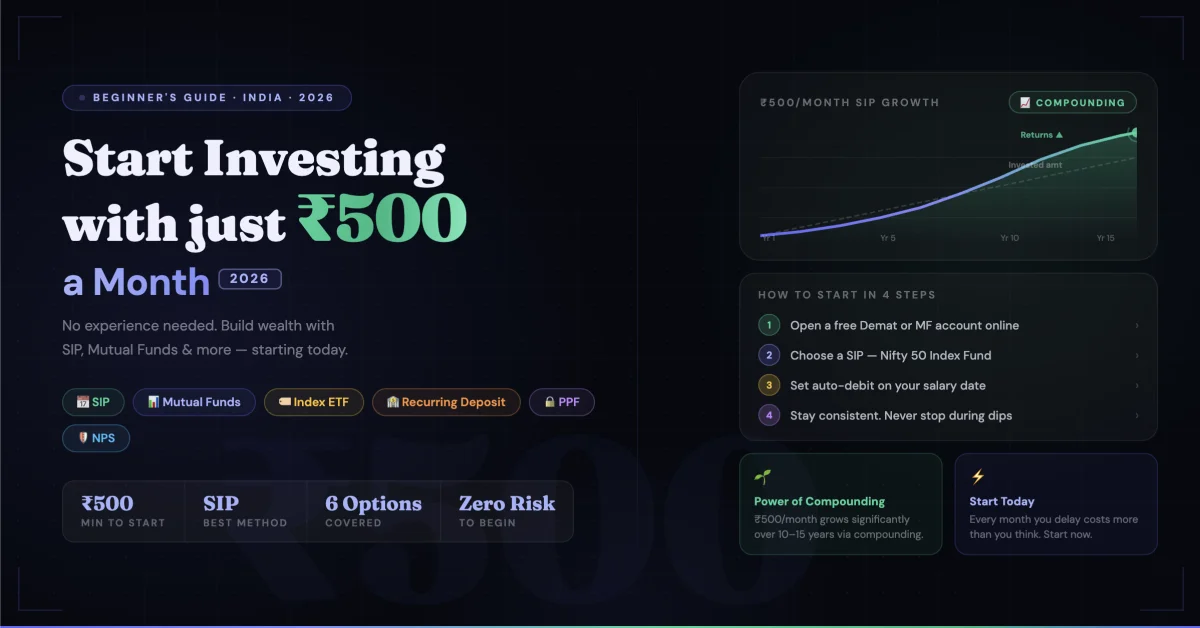

How to Start Investing in India With ₹500 a Month — The Complete Beginner Guide 2026

⚠️ Disclaimer: The information provided in this article is for general educational and informational purposes only. It does not constitute financial advice, investment recommendations, tax advice, or any solicitation to buy, sell, or hold any financial instrument, security, or product. All examples, numbers, interest rates, stock prices, and return figures mentioned are illustrative or historical in nature and do not guarantee future results. Investments in stocks, mutual funds, IPOs, commodities (gold, silver), and other financial instruments are subject to market risk. Past performance is not indicative of future returns. Tax laws and financial regulations mentioned are based on information available at the time of writing and may have changed. Readers are strongly advised to consult a SEBI-registered investment advisor, certified financial planner, or qualified tax professional before making any financial or investment decisions. RozHisab is a personal finance tracking and budgeting tool — it is not a SEBI-registered investment advisory service and does not provide investment advice.

₹500 a month. That is ₹16 per day — less than a cutting chai and a samosa at most places in India.

Most people reading this believe ₹500 is too small to matter in investing. They are making a mistake that will cost them lakhs over the next 20 years.

Here is the number that changes the equation completely:

₹500/month invested in a Nifty 50 index fund at 12%

average annual return, stepped up by just 10%

every year — becomes approximately

₹14.5 lakh in 20 years.

Your total investment: ₹3.8 lakh.

Wealth created purely by compounding: ₹10.7 lakh.

This guide covers exactly how to do this — which instruments to use, how to set up your first SIP, what a step-up SIP calculator shows you, and the traps that destroy wealth before it's built.

Why ₹500 Is Enough to Start — The Compounding Math

Before getting into the how, understand the single most important concept in personal finance: compounding. Einstein reportedly called it the eighth wonder of the world. Whether he said it or not, the math is real.

Compounding means your returns earn returns. You invest ₹500. It earns ₹60 in a year at 12%. Next year, you earn 12% on ₹560 — not ₹500. The year after that, on ₹627. And so on, accelerating invisibly for decades until the returns dwarf the original investment.

The three variables that determine your outcome:

- Amount invested — ₹500, ₹1,000, ₹5,000. More is better but you don't need much to start.

- Rate of return — Fixed instruments give 6–8%. Equity index funds have historically given 11–13% over 15+ year periods in India.

- Time — This is the variable nobody can buy back. Starting at 22 vs starting at 32 is the difference between retiring wealthy and retiring comfortably.

The correct response to "I only have ₹500" is not to wait until you have more. It is to start with ₹500 today and step it up as your income grows.

Investment Ideas for Beginners — The Right Starting Point

Before choosing a specific instrument, understand the two categories of investment available to a beginner in India:

Fixed return instruments:

Guaranteed returns, no market risk, lower long-term

growth. Examples: RD account (Post Office or bank),

Fixed Deposit, PPF, RBI Bonds.

Right for: Emergency fund,

short-term goals (1–3 years),

conservative investors who cannot sleep

if their portfolio shows a negative number.

Market-linked instruments:

Variable returns, short-term volatility,

significantly higher long-term growth.

Examples: Mutual fund SIP, Nifty 50 index fund,

Nifty BeES.

Right for: Goals 5+ years away,

wealth creation, retirement planning,

anyone who can stay invested during downturns.

The correct beginner strategy is not one or the other — it is both, in sequence:

- Build a 3-month emergency fund in an RD or liquid fund first

- Start a ₹500 SIP in a Nifty 50 index fund simultaneously or immediately after

- Step up both as income grows

Option 1 — RD Account (Recurring Deposit) — Best Fixed Return Start for Beginners

RD Account in Post Office — India's Most Underrated Beginner Account

A Recurring Deposit (RD) account is a savings instrument where you deposit a fixed amount every month for a fixed tenure and receive a guaranteed interest rate on the accumulated corpus.

RD account full form: Recurring Deposit — named because the deposit recurs every month.

RD account means: A forced monthly savings habit with guaranteed returns — the closest thing to a SIP but with zero market risk.

Post Office RD account — key details 2026:

- Interest rate: 6.7% per annum (compounded quarterly) — government-guaranteed, revised quarterly

- Minimum deposit: ₹100 per month

- Tenure: 5 years

- Tax treatment: Interest is taxable as per your income slab

- Safety: Sovereign guarantee — backed by Government of India directly

How to open RD account in SBI:

- Open SBI YONO app → go to Deposits → Recurring Deposit

- Set monthly amount (minimum ₹100), tenure (1–10 years), and start date

- Link to your savings account for auto-debit

- Confirm — RD created instantly, certificate available in app

₹500/month in Post Office RD

for 5 years at 6.7%:

Total invested: ₹30,000

Maturity amount: approximately ₹35,500

Interest earned: ₹5,500

✅ Best for: Building your emergency fund. Anyone who wants to develop the habit of monthly investing before moving to market-linked instruments. Absolutely zero risk of capital loss.

⚠️ Limitation: At 6.7%, RD returns barely beat inflation over the long term. RD is a starting point and an emergency fund vehicle — not a wealth creation instrument.

Option 2 — Nifty 50 Index Fund SIP — Best Market-Linked Investment for Beginners

What Is a Nifty 50 Index Fund?

A Nifty 50 index fund is a mutual fund that tracks the Nifty 50 index — India's benchmark stock market index consisting of the 50 largest companies by market capitalisation listed on the NSE.

When you invest in a Nifty 50 index fund, you are effectively buying a tiny piece of India's 50 largest companies — Reliance, TCS, HDFC Bank, Infosys, ICICI Bank, Kotak Mahindra, Bharti Airtel, and 43 others — in one single transaction.

Why index funds for beginners:

- No stock-picking required — you buy the whole index, not individual stocks

- Lowest expense ratio — 0.10–0.20% annually vs 1–2% for actively managed funds

- Proven long-term returns — Nifty 50 has delivered approximately 12–13% annualised returns over 20 years

- Warren Buffett's recommendation — the world's most successful investor has repeatedly said index funds are the best choice for most retail investors

- Starts at ₹500/month via SIP — no minimum lump sum required

Best Nifty 50 Index Fund in India 2026

All Nifty 50 index funds track the same index — so performance differences are minimal. The main differentiator is expense ratio and tracking error (how closely the fund matches the actual Nifty 50 returns).

- 🏆 HDFC Nifty 50 Index Fund: Expense ratio 0.20%, excellent tracking, large AUM — most reliable option. Minimum SIP: ₹100/month.

- ✅ UTI Nifty 50 Index Fund: One of India's oldest index funds, expense ratio 0.20%, consistent track record. Good for first-time investors who prefer established fund houses.

- ✅ Nippon India Index Fund — Nifty 50 Plan: Expense ratio 0.20%, strong performance history.

- ✅ Nifty Alpha 50 Index Fund (Motilal Oswal): Tracks the Nifty Alpha 50 — 50 stocks with highest alpha (outperformance) vs the Nifty 50. Higher potential returns, higher volatility — not for pure beginners, but worth knowing as a step-up from Nifty 50 after 2–3 years of investing experience.

Motilal Oswal Defence Index Fund NAV: Motilal Oswal has also launched sectoral index funds including a Defence Index Fund — tracking India's defence sector companies. Sectoral funds are NOT for beginners — they concentrate all risk in one sector. Start with a broad Nifty 50 index fund and consider sectoral funds only after building a diversified core portfolio.

What Is Nifty BeES — The ETF Alternative to Index Fund SIP

Nifty BeES (Benchmark Exchange Traded Scheme) is India's first and most popular Exchange Traded Fund (ETF) — it also tracks the Nifty 50, but trades on the stock exchange like a share rather than through a mutual fund platform.

Nippon India ETF Nifty 50 BeES is the full name. When people search "Nifty BeES share price today" they are looking at the live price of this ETF, which moves throughout the trading day exactly like a stock.

Nifty BeES vs Nifty 50 Index Fund — which is better for beginners?

- Nifty 50 Index Fund (Mutual Fund): Buy via Zerodha, Groww, or Coin app. No demat account needed for direct plans. SIP automation available. Priced at end-of-day NAV. Better for beginners — simpler setup.

- Nifty BeES (ETF): Requires demat account. Live price, trades like a stock. Very low expense ratio (0.04%). No SIP automation — you must manually buy every month. Better for slightly experienced investors who already have a demat account.

✅ Recommendation for beginners: Start with HDFC or UTI Nifty 50 Index Fund via SIP. After 1–2 years, add Nifty BeES if you want lower costs and are comfortable with a demat account.

Option 3 — Step Up SIP — The Strategy That Turns ₹500 Into Serious Wealth

What Is a Step Up SIP?

A Step Up SIP (also called Top Up SIP) is a SIP where you automatically increase your monthly investment amount by a fixed percentage or fixed rupee amount every year — matching your growing income.

This is the single most powerful wealth-building strategy available to a salaried Indian investor. Here is why the numbers are so dramatic:

Regular SIP — ₹500/month for 20 years at 12%:

Total invested: ₹1,20,000

Final corpus: approximately ₹4.9 lakh

Step Up SIP — ₹500/month,

increased 10% every year, for 20 years at 12%:

Total invested: ₹3,82,000

Final corpus: approximately ₹14.5 lakh

Step Up SIP — ₹500/month,

increased 15% every year, for 20 years at 12%:

Total invested: ₹6,50,000

Final corpus: approximately ₹24 lakh

Same starting amount. Dramatically different outcomes. The step-up is the multiplier that most people never activate.

Step Up SIP Calculator — How to Use It

To calculate your own step-up SIP projection, use any of these free calculators:

- Groww Step Up SIP Calculator: groww.in/sip-calculator — toggle "Step Up SIP" tab, enter monthly amount, annual step-up percentage, expected return rate, and tenure

- Zerodha Coin: coin.zerodha.com — has an integrated SIP step-up feature when setting up a new SIP

- ET Money SIP Calculator with Step Up: etmoney.com/sip-calculator — clean interface, shows year-by-year corpus growth

What to enter in a step up SIP calculator:

- Monthly SIP amount: ₹500 (your starting amount)

- Step-up rate: 10% per year (conservative — matches a typical annual salary hike)

- Expected return: 12% per annum (reasonable for a Nifty 50 index fund over 15+ years)

- Tenure: 20 years

Run this calculation right now. The number that comes out is your opportunity cost of not starting today.

How to Set Up a Step Up SIP in India

On Zerodha Coin:

Go to coin.zerodha.com →

search your fund →

click Start SIP →

enable "Top-up SIP" toggle →

set annual increase percentage → confirm.

On Groww:

Select fund → Start SIP →

scroll to "Step Up" →

enter annual step-up amount or percentage → confirm.

On Paytm Money:

Select fund → SIP →

Advanced Options →

Enable Step Up → set percentage → confirm.

Most platforms allow you to set step-up as either a fixed rupee increase (increase by ₹100 every year) or a percentage increase (increase by 10% every year). Percentage step-up is better — it scales automatically as your base amount grows.

Option 4 — Gold Investment for Beginners

How to Invest in Gold for Beginners in India

Gold is India's most culturally familiar investment — but most Indians invest in it in the worst possible way: physical gold jewellery with 15–25% making charges that evaporate the moment you buy.

The right way to invest in gold for a beginner with ₹500:

1. Digital Gold (Quickest to start):

Buy via PhonePe, Google Pay, or Paytm —

as little as ₹1 worth of gold.

Stored in secure vaults,

can be sold anytime at live gold prices.

Use only for amounts under ₹10,000 —

not regulated by SEBI,

so not appropriate for larger holdings.

2. Gold ETF (Best for ₹500–₹5,000/month):

Same as Nifty BeES but for gold.

Nippon India Gold ETF, HDFC Gold ETF,

SBI Gold ETF — all track physical gold price.

Requires demat account.

Expense ratio: 0.40–0.59%.

Buy as little as 1 unit (~₹60–₹70 currently).

3. Sovereign Gold Bond — SGB

(Best for 5+ year horizon):

Issued by RBI, backed by Government of India.

Earns 2.5% interest per year on top of

gold price appreciation.

Minimum: 1 gram (~₹7,000–₹8,000 depending

on issue price).

Best long-term gold investment available —

but requires a minimum of ₹7,000 upfront,

so not suitable for the ₹500/month beginner immediately.

Save for 12–14 months, then buy one SGB unit.

✅ Beginner gold strategy: Start with Digital Gold on PhonePe at ₹100–₹200/month while building your Nifty 50 SIP. After 1 year, switch to Gold ETF. After 2–3 years, buy SGBs with accumulated savings.

The Mutual Fund SIP Setup — Step by Step for a Complete Beginner

Mutual Funds Investment Plans for Beginners — Exact Setup Guide

Step 1 — Choose your platform

Groww (easiest for beginners —

clean UI, guided fund selection,

app available on Android and iOS)

Zerodha Coin (best if you'll

also invest in stocks later —

one demat for everything)

Paytm Money (good if already

a Paytm user — familiar interface)

Step 2 — Complete KYC

One-time process.

Takes 10–15 minutes.

Required documents: Aadhaar + PAN +

selfie + bank account details.

Done entirely online on any of the above platforms.

KYC is a one-time process that works

across all mutual fund platforms in India

once completed.

Step 3 — Choose your first fund

For a complete beginner investing ₹500/month:

HDFC Nifty 50 Index Fund — Direct Plan — Growth option.

Direct Plan = no distributor commission

(0.20% expense ratio instead of 0.80%+ for regular plan —

this difference compounds to lakhs over 20 years).

Growth option = returns compound back into the fund

instead of being paid out as dividends.

Step 4 — Set up SIP

Amount: ₹500

Date: 5th of every month

(salary usually credited 1st–3rd —

invest before you spend)

Step-up: 10% annually

Duration: Until retirement (no end date)

Step 5 — Set up auto-debit

Register your bank account for NACH auto-debit.

This ensures the SIP deducts automatically

every month without you having to remember

or log in. Automation is the single

most important habit in SIP investing.

A forgotten SIP is a missed compounding month.

⚠️ How to Invest in Mutual Funds for Beginners — What NOT to Do

Penny Stocks — The Biggest Beginner Trap

Every month, thousands of new Indian investors search for penny stock lists, top 10 penny stocks in India, and multibagger penny stocks — hoping to turn ₹500 into ₹50,000 quickly.

Here is the honest truth about penny stocks:

92% of retail investors who trade F&O and penny stocks lose money — per SEBI's own published research. The number for penny stock traders specifically is even higher because penny stocks are the preferred instrument for pump-and-dump operators.

A penny stock that goes from ₹2 to ₹20 sounds like a 10x return. But here is what actually happens: operators accumulate at ₹2, push to ₹20 with social media hype, retail investors buy at ₹15–₹20 on FOMO, operators dump, stock crashes to ₹3. Retail investor is down 80%.

₹500 in a Nifty 50 index fund:

Virtually guaranteed positive returns over 10+ years.

Historical worst case: temporary loss

during a crash, full recovery within 1–3 years.

₹500 in penny stocks:

Real probability of losing 50–80% permanently.

The search for multibagger penny stocks is the search for a shortcut that doesn't exist. The only shortcut in investing is starting earlier.

Best Earning App Without Investment — The Myth

Searches for "best earning app without investment" and "daily ₹100 earning app without investment" represent a genuine pain point — people want to build wealth but believe they don't have enough to invest.

The honest answer: there is no app that generates meaningful passive income without any capital or effort. Every such app either pays ₹2–₹5 per task (below minimum wage for the time invested), requires you to refer others (MLM structure), or is an outright scam.

The real "earning without investment" strategy: Your human capital — skills, education, career — is your most valuable asset in your 20s and 30s. Invest in skills that increase your income by ₹2,000–₹5,000/month. That extra income, invested in a Nifty 50 index fund, is worth far more than any "earning app."

₹500/month is enough to start. Start with ₹500. Step it up as your income grows. That is the only system that works.

How to Invest ₹500 a Month — The Complete Beginner Allocation

Here is the exact allocation for someone starting with ₹500/month total to invest:

If you have NO emergency fund yet:

→ ₹500/month into Post Office RD or

SBI RD account until ₹15,000–₹20,000 saved

→ Then split: ₹300 Nifty 50 SIP + ₹200 RD

(continue building emergency fund)

→ Once emergency fund complete (₹30,000–₹40,000):

₹500 fully into Nifty 50 SIP

If you already have an emergency fund:

→ ₹400 — Nifty 50 Index Fund SIP

(HDFC or UTI Direct Plan Growth)

→ ₹100 — Digital Gold via PhonePe

(builds toward first SGB unit)

Step-up plan:

Year 1: ₹500/month

Year 2: ₹550/month (10% step-up)

Year 3: ₹605/month

Year 5: ₹733/month

Year 10: ₹1,179/month

Year 20: ₹2,909/month

Your SIP amount has nearly 6x'd — automatically — while your monthly burden has only grown modestly each year. This is step-up investing in action.

Track Every Rupee You Invest — From Day One

Here is the mistake that even disciplined investors make: they set up the SIP, forget it, and have no idea what their actual invested amount or current corpus value is after 3 years.

When you don't track, you make two errors:

- You redeem at the first sign of a market dip because you don't see the full picture (you're down 12% this month but up 87% overall)

- You miss your step-up dates because there's no system reminding you to increase

Use RozHisab to log every SIP investment alongside your monthly income and expenses. See your running investment total, monthly savings rate, and how much of your income is actually being invested — all in one free dashboard built for Indian users.

When you can see that your ₹500/month SIP has grown to ₹18,000 over 3 years of investing — the market dip that tempts you to redeem becomes easy to ignore. Visibility creates patience. Patience creates wealth.

👉 Start investing with ₹500 today.

Track it on RozHisab

from day one.

Step it up 10% every year.

Don't touch it for 20 years.

That is the complete strategy.

Everything else is noise.

Quick Reference — ₹500/Month Investment Guide

- 🏦 Emergency fund first: Post Office or SBI RD — ₹500/month until ₹30,000 saved

- 📈 Core investment: HDFC or UTI Nifty 50 Index Fund — Direct Plan, Growth — ₹500 SIP

- ⬆️ Step-up: 10% increase every year via Step Up SIP calculator and auto step-up

- 🥇 Gold allocation: ₹100/month Digital Gold → switch to Gold ETF after 1 year

- 🚫 Avoid completely: Penny stocks, F&O trading, "earning apps without investment," ULIPs sold by insurance agents

- 📱 Best platforms: Groww (beginner), Zerodha Coin (advanced), Paytm Money (familiar)

- 📊 Track everything: Log all investments on RozHisab — free, built for Indian households

- ⏰ Most important rule: Start today. Not next month. Every month of delay costs you compounding you can never get back.

Track your own finances — free forever

Use RozHisab to apply everything in this article to your actual spending and savings.

Start Tracking Free →